WaFd made it a priority to invest in cutting-edge fintech solutions — tapping into the full suite of MX products and creating its own innovation lab that is now Archway Software, an independent SaaS company.

“My very first meeting with MX, I asked them to fly everyone up to Seattle and we called it Nerd Fest,” said Dustin Hubbard, Founder and President, Archway Software. “It was three days of being locked in a room and whiteboarding out the architecture that we’d ultimately go on to build. And MX being MX, they actually showed up with Nerd Fest T-shirts that I still have. They’re awesome! So that’s kind of where the relationship started.”

At the time this journey began, WaFd was one of the nation’s top six banks when it comes to shareholder return and saw consistent, steady market growth. However, the bank was keenly aware that any big changes could put that success at risk — while doing nothing was likely an even bigger risk.

“We were pleased with our track record,” Beardall says. “But that also scared me to death because it’s easy to get complacent. It’s human nature to be conservative and not want to mess up a really good thing. But that’s a real risk today — that we just fall in love with who we were in the past and fail to innovate and be proactive in meeting our customers’ current needs.”

To distinguish itself and deliver a better money experience for consumers today and tomorrow, the bank knew it had to innovate and offer something better. Beardall admits developing an entire independent SaaS company to equip themselves for the future was a bold move, but that decision coupled with the collaborative nature of its partnership with MX, paid off in full for WaFd and its customers. Now unencumbered by long-term contracts with slow-moving vendors, WaFd can control its data, own its middleware, and be more selective about what vendors it uses. This hard-won freedom — to innovate and build on its own terms — is at the heart of WaFd’s journey.

Another key element of WaFd’s journey is its flexibility to partner with forward-thinking fintechs to provide its customers with leading technological solutions. The relationship between WaFd and MX is one example. WaFd purchased MX’s full suite of products, including Financial Insights, which provides smart, AI-powered insights to help users increase its financial strength.

Partnering with MX gave WaFd access to tools that help it uncover important financial health insights within its data. For instance, MX allowed the bank to see that roughly 44% of its clients using MX’s money management tools were classified as “financially vulnerable.”

And, with account aggregation powered by MX, WaFd is able to gain a deeper understanding of its customers’ full financial picture with visibility into more than 6,500 external accounts that its customers have connected to the WaFd banking experience.

“MX aggregated accounts — this is a huge miss I’ve seen with banks where the client is connecting their accounts on their banks. As a client, I can see all of my accounts but the banks weren’t really doing anything meaningful with that information,” said Hubbard.

With these insights, WaFd can better target and reach specific customer segments with the right products and services that can empower them to strengthen their financial health. Consumers are also able to see a more comprehensive view of their finances in one place, enabling a better end-user experience in managing their day-to-day finances.

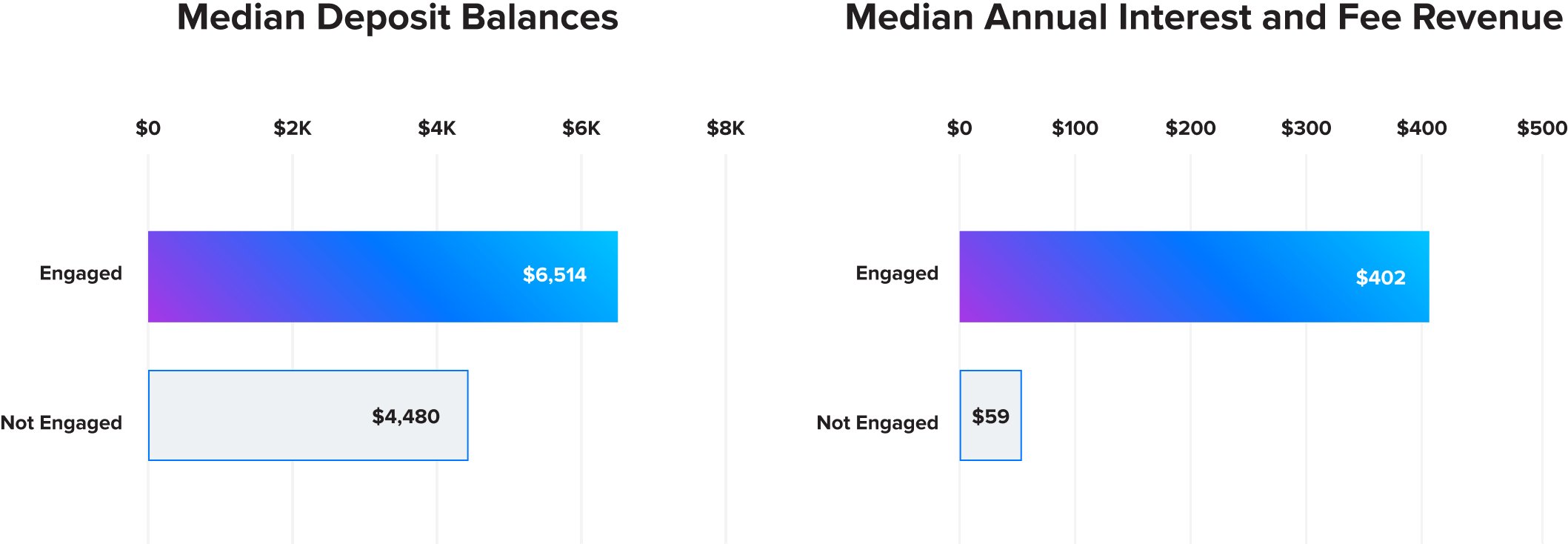

In fact, WaFd consumers who engage with MX’s tools have a significantly higher median deposit balance ($6,500) than those who don’t use them at all ($4,500). Those who are engaged with MX tools have also led to higher returns for the bank. This is a strong indicator that investing in an experience that supports financial health pays dividends in loyalty and wallet share.

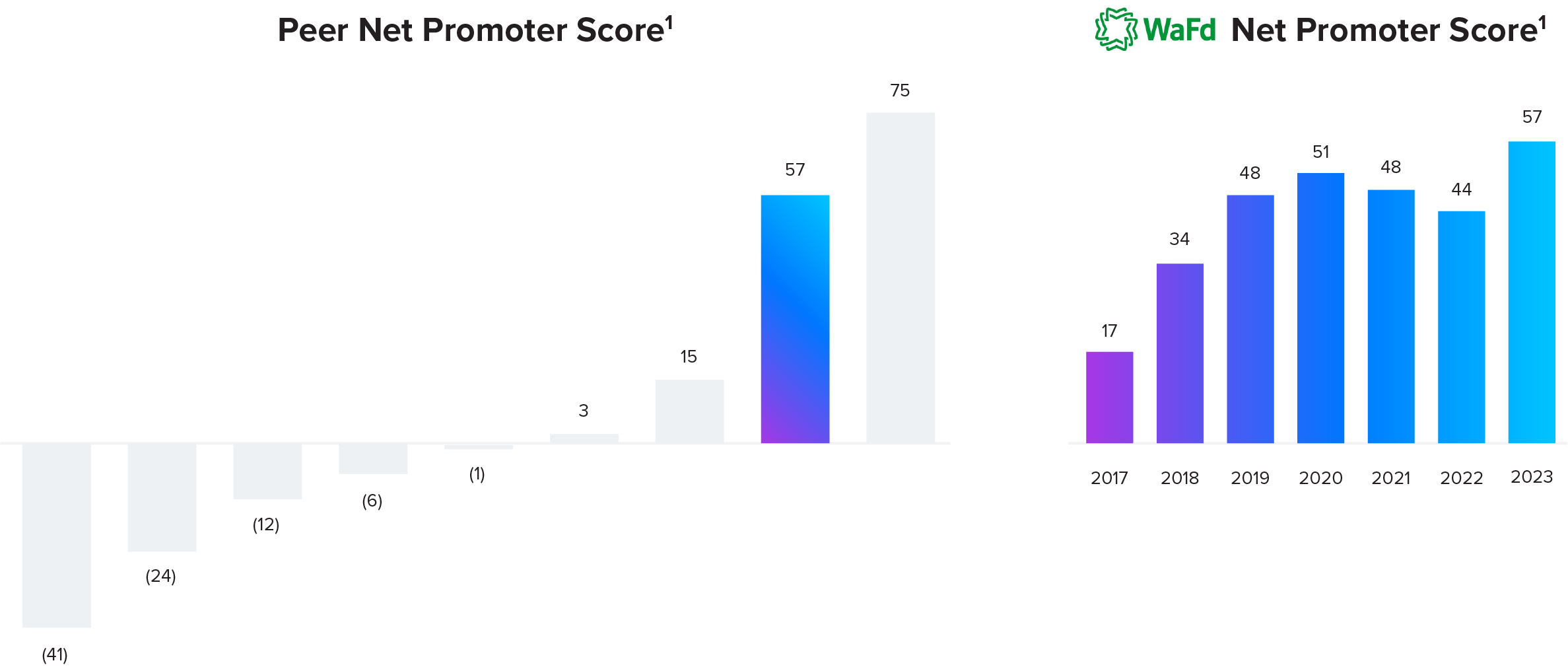

As a result of WaFd Bank’s focus on innovation and leveraging data to drive value for consumers, customer satisfaction has soared. Since this journey began, the company’s Net Promoter Score has increased exponentially, achieving a current score of 57 — significantly higher than the industry average (24) for banks.

“I’m a big believer in Net Promoter Score. Five years ago, WaFd was at 17. This last year, we’re up to a 57 Net Promoter Score,” said Beardall. “That is phenomenal. And, we’re just scratching the surface of what we can do with technology now.”