From Stability to Security: Understanding the Financial Hierarchy Shaping Consumer Behavio...

April 24, 2026 | 5 min read

MX research shows how consumers prioritize aspects of their finances in a financial hierarchy.

Copied

Aug 11, 2020|0 min read

As part of our ongoing research on what consumers want from banks and fintech companies — featured in our ultimate guides — we recently took a dive into financial account aggregation.

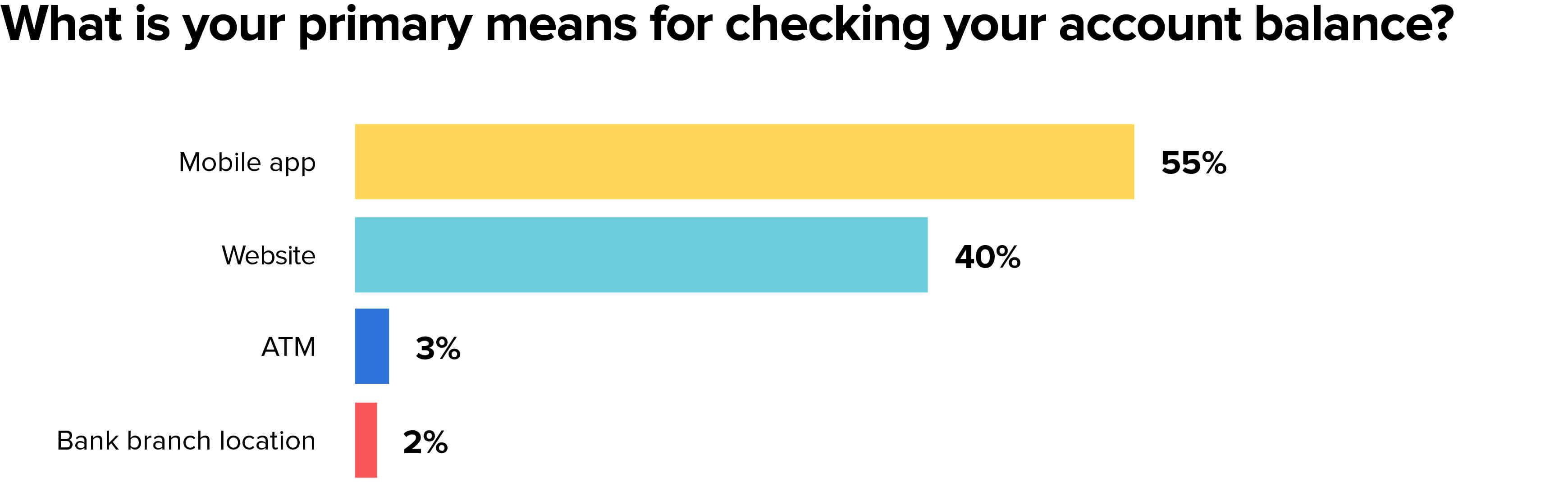

First, we asked people about their primary means for checking their financial account balance and found that 95% of people use a digital channel: 55% say mobile, 40% say website.

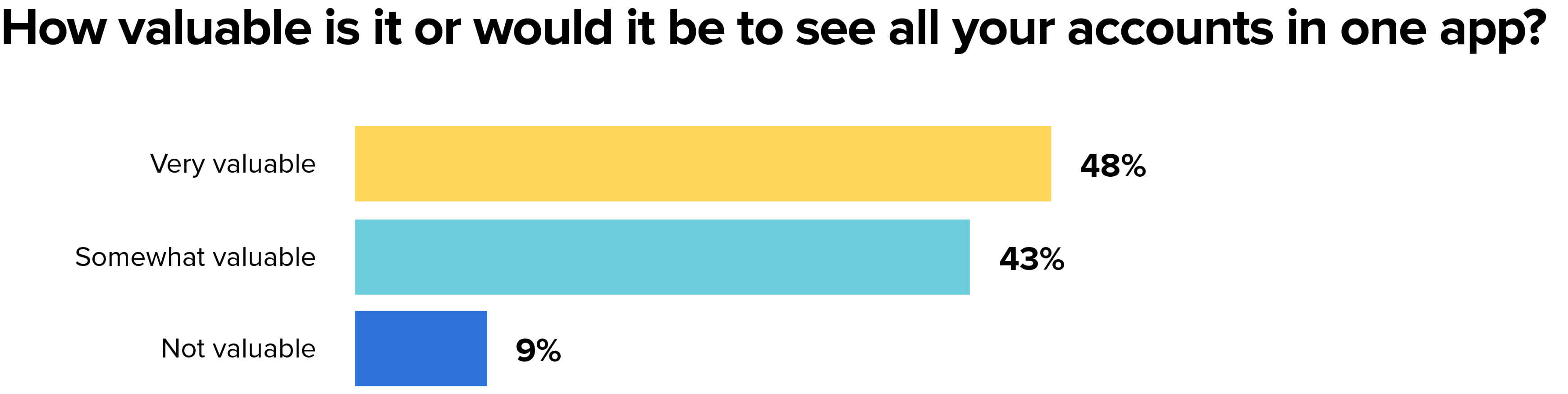

Second, we asked people how valuable it is (or would be) to see their financial accounts in one app. Nearly half (48%) said that it would be very valuable, while nearly the same percentage (43%) said it would be somewhat valuable, adding up to 91%.

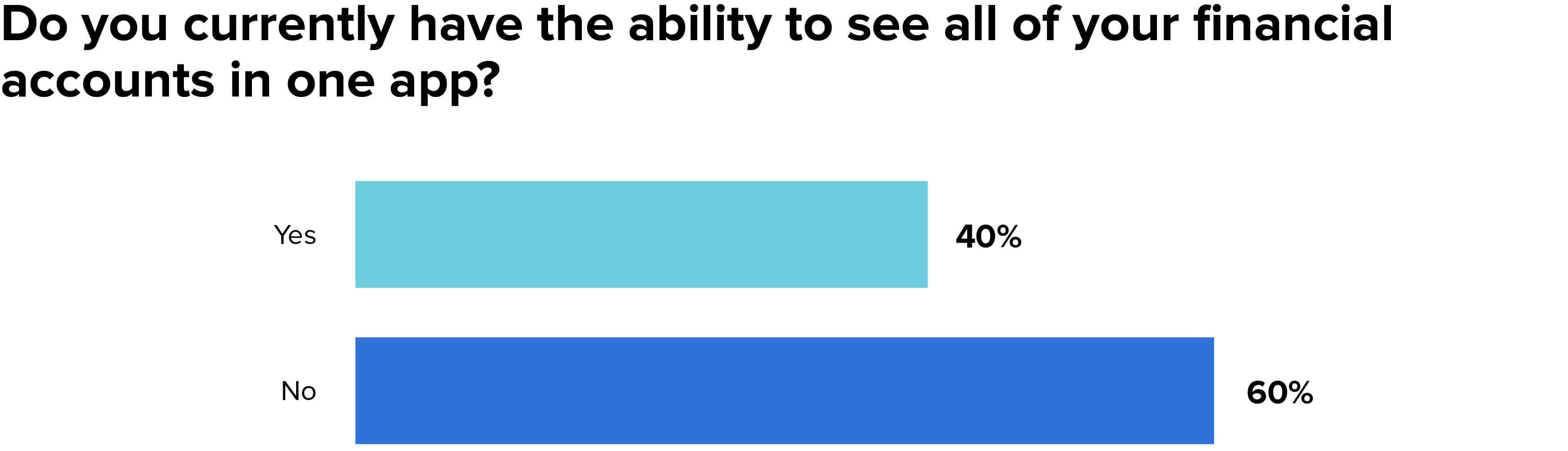

Despite the overwhelming majority who said this feature would be valuable, only 40% said they could currently do it.

This represents a remarkable disconnect between what consumers and what financial organizations are providing them.

Put simply, people want the ability to sign into a single place and see everything —checking, savings, car loan, mortgage, 401(k), etc. — in one view. They want to see balances and transactions together so they don’t have to sign into a separate account to get a full sense of their finances.

And yet financial organizations still haven’t fully implemented solutions on this front, as evidenced by the 60% of consumers who say they don’t have this ability.

What these organizations might not realize is that enabling customers to see all their data in one place also benefits them in the form of being able to gather a 360-degree view of each customer’s financial life. In this way, financial organizations can better understand their customers and make hyper-relevant offers that meet each customer where they are. It also gives financial organizations insights against direct competitors each time a customer aggregates a financial account from that competitor.

Traditionally, aggregation has happened via screen scraping from third parties that don’t have a formal relationship with the organization they scrape from. However, this process is quickly changing today, as more organizations are shifting to whitelisting data aggregators and implementing direct APIs. These new options bring many benefits to financial organizations that previously didn’t exist, including added transparency, clearer permissions, and increased security.

As more financial institutions implement APIs, direct aggregation methods will become standard. This move will enable increased innovation since customer-permissioned data sharing is often bi-directional, meaning that financial institutions and fintech companies can share and receive data from the sources they connect with via API. This capability sets up all parties involved to use that data in creative ways to best serve and advocate for their customers.

Above all, this customer-centered approach to banking is at the heart of where things are headed. And that’s terrific news for the 91% of consumers who value account aggregation — as well as the financial organizations who offer it.

Want to see more consumer research about connectivity? See our Ultimate Guide to Fintech Data.

April 24, 2026 | 5 min read

April 14, 2026 | 7 min read

April 1, 2026 | 3 min read