An Inside Look at the Money Experience Leadership Forum

Feb 9, 2026 | 2 min read

At the Money Experience Leadership Forum, financial leaders discussed how to find paths to growth across the industry.

April 28, 2020|0 min read

Copied

As part of our ongoing series to highlight specific presentations from Banking Transformation Week, we want to feature Ron Shevlin, Senior Contributor at Forbes and Managing Director at Cornerstone Advisors. Ron presented on five debates that will shape the future of banking.

You can watch the video or read the transcript below.

If you thought there were a lot of changes in banking and fintech last decade, you ain't seen nothing yet compared to what we're going to see in the 2020s.

Now, I don't know exactly what's going to happen in banking in fintech in the coming decade, but I do know this: We're going to be wrestling with a number of big debates, and there are five debates in particular that we're going to wrestle with in the 2020s.

1. Branches: Are they dead or alive?

2. Artificial intelligence: Is it inherently biased and in need of regulation?

3. Data privacy: Is there a balance that we can achieve?

4. Superapps: Are they coming to the US?

5. Cryptocurrency: Are they going to have an impact or not?

So let's look at each of these five debates for the next decade.

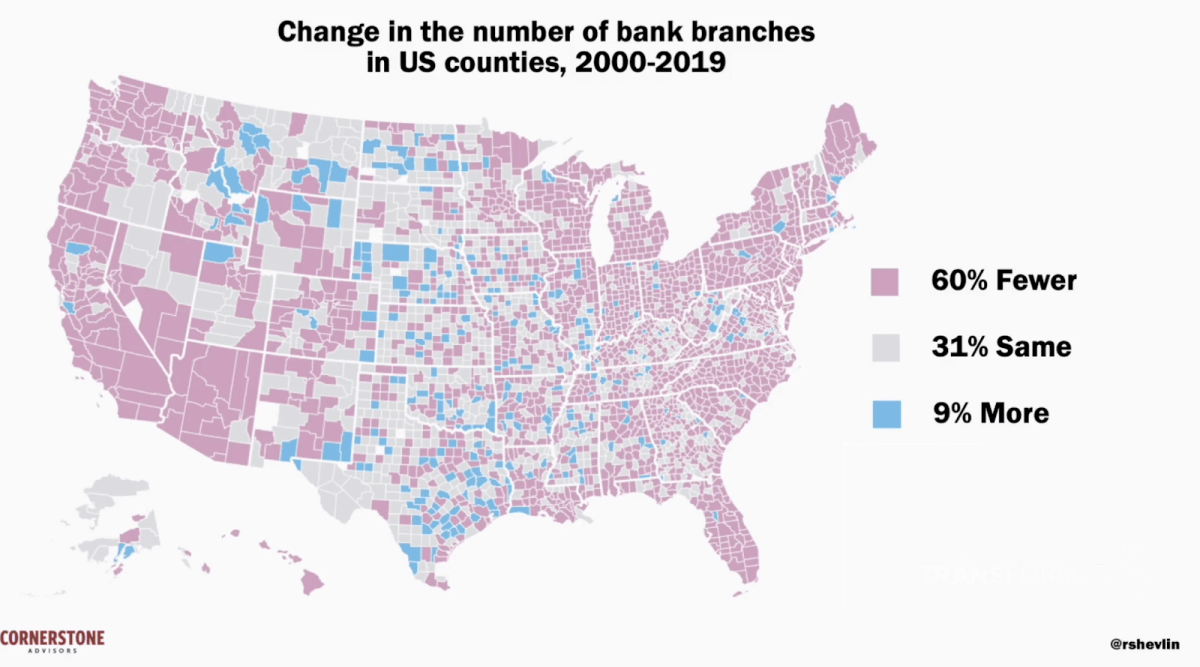

First up, our branches, are they dead or alive? Well, clearly the numbers show that there's a downward trend in branches.

If we look at this from a geographic perspective, 60% of the counties in the US have experienced a decline in the number of branches over the past 20 years. Only 9% have seen an increase, but the people who support the branches say, “Well that's not the real story. The real story is that we're reinventing the branches that we're going to resize them.” You see a lot of articles that say bank branches are evolving and shrinking and so forth, but reality is the exact opposite. A study from JLL found that in both the Northeast and West, the average new project size of branches is actually greater than it is of the existing size of branches. Now, while the new projects in both the South and Midwest are smaller, take note that the average branch sizes of those new projects are both larger than they are of the existing branches in both the West and the Northeast.

The branch supporters like to point to examples like what Chase has done. They've opened up 12 new branches in the year or so along the Northeast and Atlantic seaboards in Washington, Boston, Philadelphia, and Delaware. And of the 12 branches that they've opened up, six have already gathered more than $25 million in deposits, which is generally the accepted level of breaking even. And in fact the branch in Boston has amassed more than a hundred million dollars in deposits. This gives a lot of the branch supporters ammunition to say that branches are still alive. But those numbers pale in comparison to what Marcus has been able to acquire with no branches over the past few years— currently about $60 billion in deposits. So the real debate that we're going to have over the next few years is not really about whether branches are dead or alive.

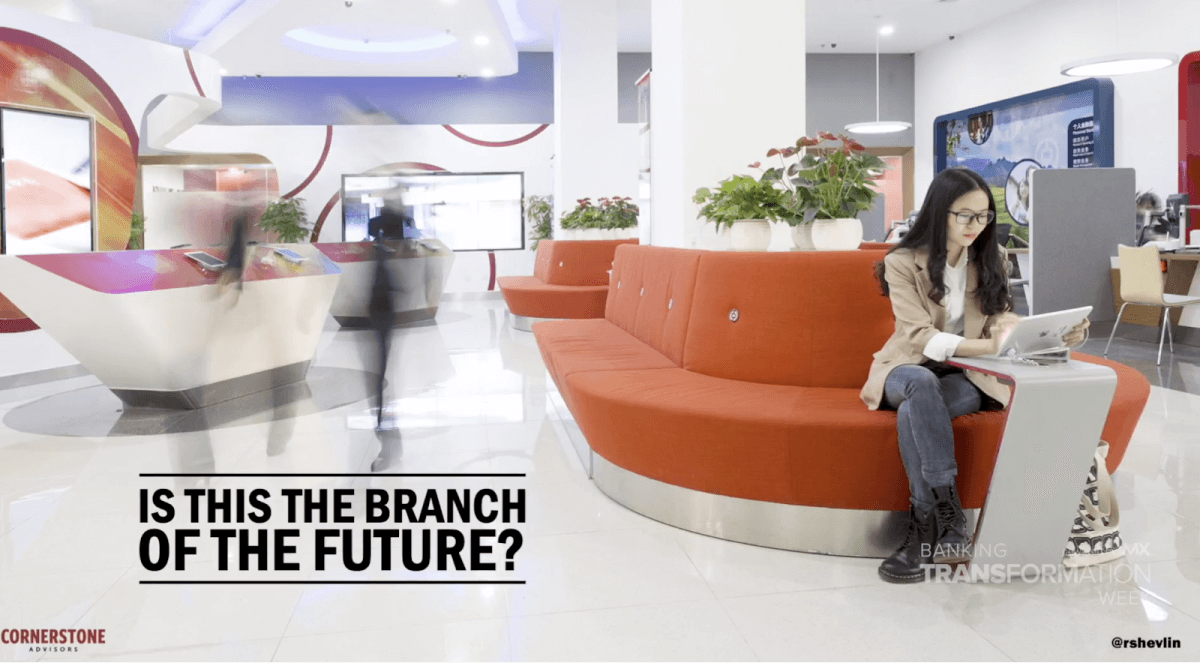

The real debate is going to be what are the branches going to look like and what role would they play? The real debate is going to come down to this:

Is this the branch of the future?

Or is this the branch of the future?

Many bankers say that their branches are for personal interaction. But the reality is that the smartphone is probably a better tool to enable person-to-person engagement than somebody having to get up and go down to a bank branch. Why do we need all of this technology in the branch when people have access to that technology in the home?

I'd like to throw out a third example. Perhaps the bank or the future or the branch of the future actually looks just like this — just a desk and some chairs with some ability for people to talk to each other.

The other reason why this is gonna be such an important debate, for the next couple of years and throughout this decade, is the community aspect. In communities where branches are closing, people are stepping up and saying, “No more. We need access to banks. We need access to the branches.” So we're going to continue to see this as one of the key debates for the 2020s.

The second key debate is going to center around artificial intelligence and whether it’s inherently biased and in need of regulation. You know, to an extent I find this to be a red herring argument because it really isn't about technology. It's about the use of data. And without a sufficient amount and quantity of quality of data, AI is pretty much useless. But there are folks like Karen Hao who wrote recently in MIT Technology Review that bias can creep into AI tools and technologies long before the actual data gets brought to the table.

And of course, we know that the Apple card got some criticism because of potential bias in its algorithms. This hasn't stopped the CEO of Google from coming out and saying that AI must be regulated, but I think we're in the next couple of years we're going to see a debate over this because what's really happening is the assimilation of AI. What's happening is that the parts of systems and tools that are AI based are becoming indistinguishable from the other parts. And as we continue to evolve to a cloud based environment, the sources of data are becoming harder and harder to track. We're incorporating data from many different sources. And so the ability to regulate and figure out exactly the source of potential biases is getting to the point where it's going to be practically impossible to regulate AI. But that's not going to stop the debate.

Debate number three: data privacy. Is there a balance achievable? You know, I talk to a lot of financial institutions, and one of the things I like to ask them is, “Do you believe that personalization is critical to your organization's success?” And most executives agree that it is. But if you think about what type of customer data you need to to do personalization, it spans a lot of different types of elements from, of course, things like demographics and transaction history and credit scores, but to things like response, propensity, purchase intention, channel behavior, and even social graph and social media data.

This is coming from a lot of different places, and we're getting to the point from a cultural perspective where it was kind of saying, “Enough is enough.” People are raising the fears of surveillance capitalism. One particular report I saw recently that really resonated was a report on the downsides of personalization, pointing out how personalization can lead to things like exploitation, manipulation, marginalization, and even things like injustice and narcissism.

The key problem here really has to come down to how we think about what personalization is. Personally, I think about it more in terms of conversations and relationships. Think about it: When you're out on that first date, there are things that you wouldn't say to people because you don't really know them very well. And even if you did, you don't feel comfortable saying them. But after you've had a relationship with somebody for 30, 40 years, there are certain things you can say. So data privacy really relates a lot more to the stage of relationship that we have with customers that banks and credit unions have with customers. But we're going to be facing a debate over whether or not that balance can be achieved over the next couple of years.

Debate number four are super apps coming to America. For those of you who don't know what super apps are, they're very popular in China. Basically think about them as a Swiss army knife of applications all under a single organizational banner. So instead of like today where you have 30, 40 different apps on your cell phone, you'll still have that many number of apps, but they'll all be tightly interconnected, with a single organization.

WeChat has over a billion customers in China, and more than half of them spend 90 minutes or more on that app every day. The challenge in the U.S. is not just whether or not Chinese apps or super apps are coming to the country, but what happens with the big tech apps. You know, 70% of the credit unions and banks that I surveyed recently said that tech companies are a significant threat in the coming decade, but for them to be able to deploy super apps and have them really take hold in the U.S. really or, or depends upon some cultural changes as well as political and organizational changes.

Will the U.S. adopt socialistic economic approaches like they have in China? Will their social credit system like Zen place in China, take hold in the US and will cultural changes in the U S support super apps today? I think that's the American credo to have best of breed and want choice. But is that changing in the US? It may very well support an environment where super apps, whether they come from the Chinese companies or not, will take hold and really impact how a financial services firm operates. And especially how they market.

The last debate I want to talk about is cryptocurrencies. Are they going to have an impact or not? If you look over the past couple of years and look at Bitcoin transaction volume, you can see a huge spike back in 2017 in terms of the amount of transaction volume and trading volume.

To give you a sense of perspective of how much is being traded and transacted in Bitcoin in 2018, the amount of $1.3 trillion is double the amount of transactions done through PayPal and almost four times as much that Discover credit card did. And of course we're seeing governments like the US and China in particular begin to eye issuing their own cryptocurrencies.

But I think the real potential impact, and where the debate around cryptocurrency is really gonna come into play, is around whether or not the corporate sponsored cryptocurrencies are going to take hold. Of course, last year we saw the introduction of Facebook's Libra with many very high profile companies being affiliated with that association. It didn't take very long for a number of those companies to bail out of Facebook's association. But examples like Facebook, JP Morgan chase with its coin and Walmart with its cryptocurrency really are going to form the basis of this debate whether or not the corporate led cryptocurrencies can take hold, which will have a huge impact on financial institutions, payment, revenue streams, payments offerings, and so forth.

So these are the five big debates we're going to see in the 2020s around bank branches. Are they alive or not? And what they're going to look like. Artificial intelligence is inherently biased and cannot be regulated, even if it is data privacy. Can we achieve a balanced super app? Are they coming to America or not? And cryptocurrencies, are we going to see the impact or not?

Feb 9, 2026 | 2 min read

Jan 15, 2026 | 4 min read

Jan 9, 2026 | 3 min read