The Great Wealth Transfer Is No Longer a Forecast. It’s Your New Retention Strategy.

April 28, 2026 | 3 min read

The "Great Wealth Transfer" is coming — and it's something financial institutions need to be prepared for.

Copied

Aug 20, 2020|0 min read

If history is a sign of things to come (and it is, as you’ll see below), companies that ignore fintech do so at their own peril. Luckily, there’s still time to get ahead of the curve and start innovating. Forward-looking financial institutions will reap rewards for years.

Here’s why:

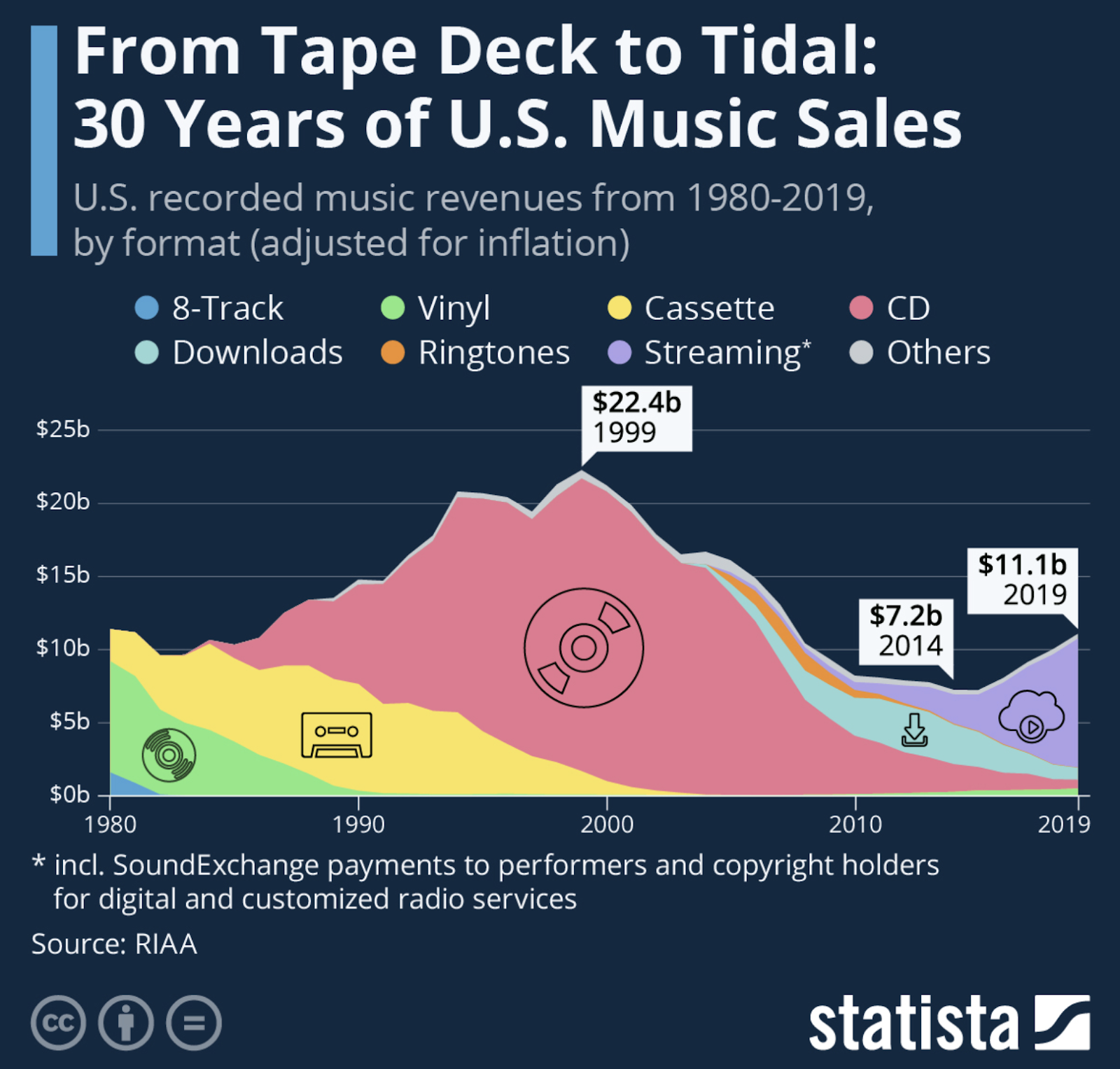

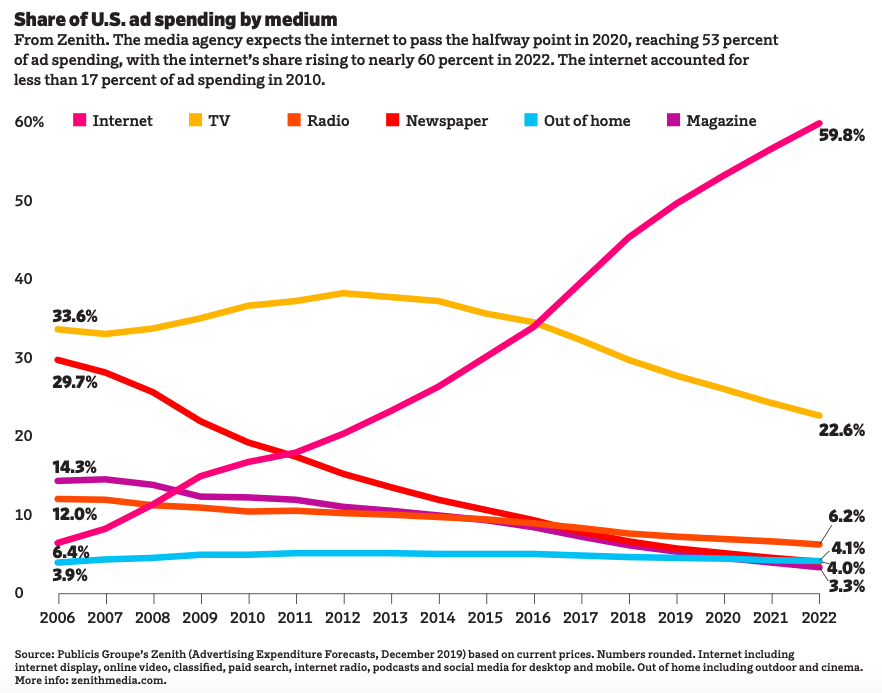

Digital technology has revolutionized industries worldwide. Consumers now demand digital music instead of CDs and online media instead of newspapers.

What’s surprising is how quickly the change occurred.

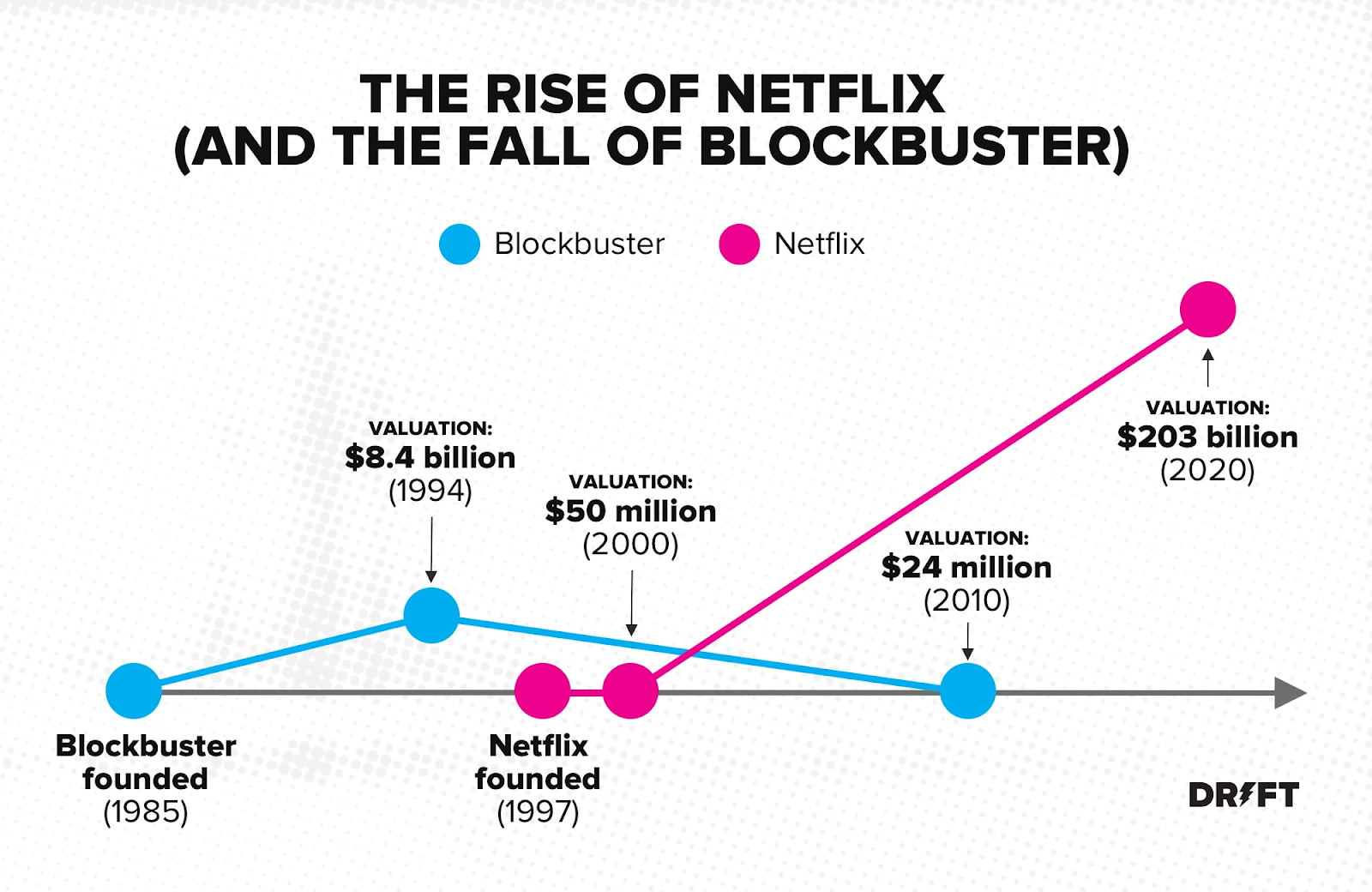

Look at the book industry for example. In less than eight years, Amazon went from underdog to powerhouse and knocked Borders out in the process.

Today’s consumers have adapted. They’re not only accustomed to the digital revolution — they expect it, along with all the conveniences it brings.

It’s the same repeating story:

(Note that everything on this graph after 2019 represents predictions from Zenith Media.)

Simply put, companies such as Borders and Blockbuster were slow to adapt to the digital revolution and were unable to recover, while industry pioneers like Amazon and Netflix saw the shift as an opportunity. By adapting to new consumer expectations, these digital pioneers delivered exactly what users demanded.

'In the next 10 years, we’ll see more disruption and changes to the banking and financial industry than we’ve seen in the preceding 100 years.” — Brett King

There has been an enormous shift in asset concentration and customer loyalty during the past two decades. For instance, the 10 biggest banks in the US now have more assets than all other lenders combined.

One reason for this shift is that the biggest banks have made banking more convenient. They’ve better met the demands for robust online and mobile offerings.

Take Bank of America, for instance. Bank of America was the first financial institution to launch mobile banking on the iPhone, and the results were impressive. More than six million people downloaded the app, and according to their data, a quarter of a million joined Bank of America specifically to use mobile banking.

All this growth came despite the fact that during that same time period Bank of America was deemed as the main villain during Bank Transfer Day in November 2011 (a grassroots movement to switch from big banks to credit unions). What’s more, at the time they scored the lowest of any financial institution on a customer satisfaction survey — 11 percentage points below the industry average. Regardless of those scores, they drew in new customers because they led the way on mobile banking.

In retrospect, Bank of America’s user growth might not be surprising. After all, Bank of America simply gave users what they wanted: Convenience.

And, to put it bluntly, convenience is king.

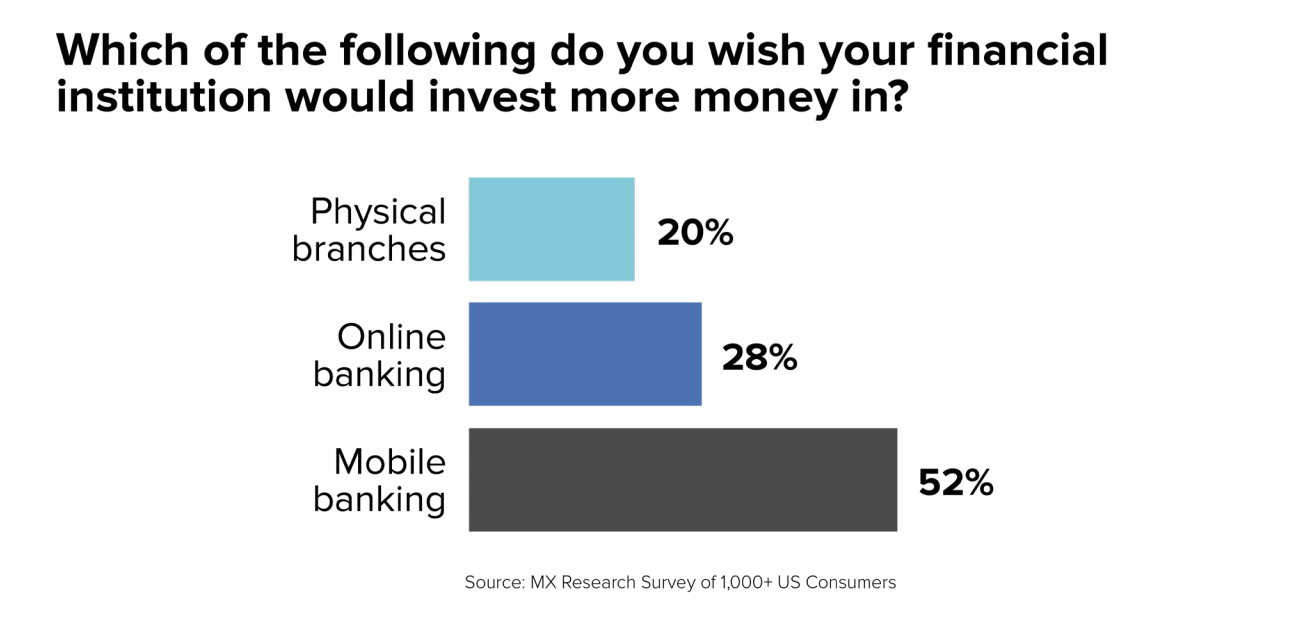

When asked what attributes they want most in a financial institution, users say they want digital solutions.

It follows that when financial institutions focus primarily on customer service at the expense of digital convenience, they risk losing their user base. Having a friendly staff and being involved in the community isn't enough. Users demand convenience, and companies that don’t meet user demands don’t survive.

All of this illustrates the necessity of investing in fintech, especially since the volume of transactions handled at a physical branch has declined by more than 45 percent across the industry since 1992, while the cost per teller transaction has skyrocketed.

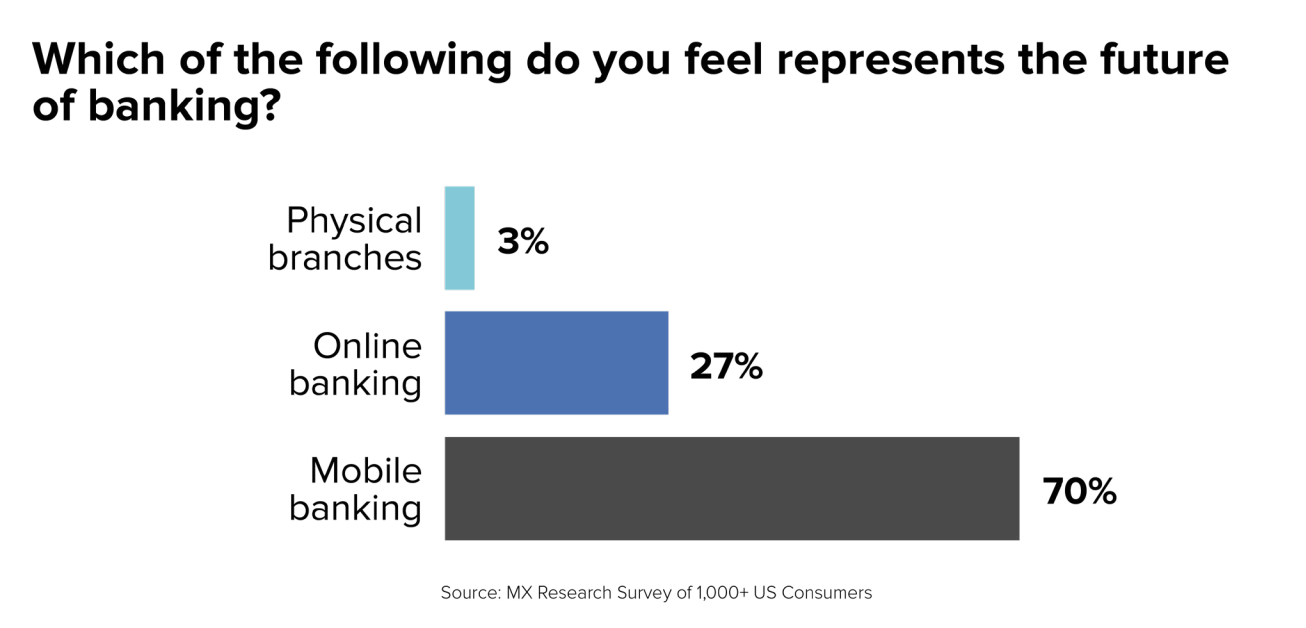

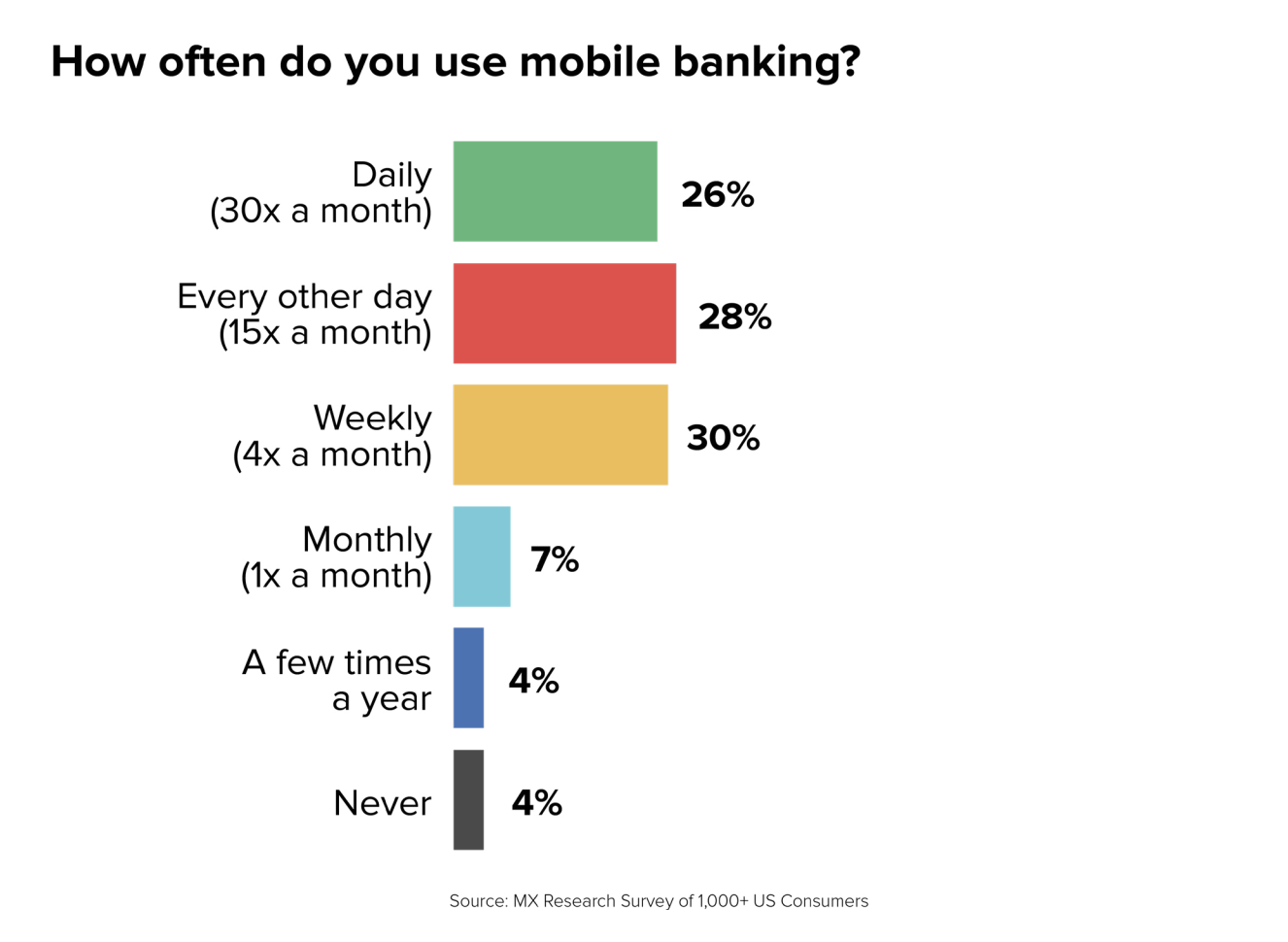

In other words, focusing primarily on a traditional growth model (e.g., building branches and hiring new tellers) is merely an expensive way to fail. In addition, the revolution in the financial industry is not slowing down, as evidenced by the sharp decline in transaction volumes. If anything, the change is speeding up. Users are visiting physical branches less and less, and they’re demanding digital channels more and more, with more 80% of consumers saying they use mobile banking at least weekly.

It’s not a surprise, then, that a host of new digital players such as PayPal, Chime, Simple, and Google have moved into the financial space. Along with innovative big banks, these disruptive companies and technologies could be viewed as the Amazons and iTunes of the financial industry — innovators that represent a tremendous threat to smaller market players.

Eventually, these disruptive companies will give their users the option to do everything digitally. Given this option, why would users choose to drive to a branch, wait in a line, sign a paper deposit slip and get a receipt? If users increasingly avoid similar experiences when purchasing books, music, movies and news, why would they choose something different for banking?

The answer is simple. They wouldn’t.

In sum, it’s clear that when financial institutions don’t innovate alongside their competitors, they risk stagnated growth (like Barnes & Noble) or going bankrupt (like Borders). Keep in mind that only one generation needs to make the switch to digital banking en masse, and the traditional model will be irrelevant.

And that’s why fintech is so crucial.

April 28, 2026 | 3 min read

Feb 9, 2026 | 2 min read

Jan 15, 2026 | 4 min read