Introduction: Digital Transformation

As the banking industry goes through a digital transformation, two deep currents are driving changes within the global financial services ecosystem:

1. More choice. People can search for a phrase such as “home loan” or “high-interest savings account” and immediately scroll through hundreds or even thousands of options — many of which are directly available via their digital device. Decisions aren’t restricted by locality or by traditional banking hours.

2. Less friction. People no longer have to walk into a banking branch to change how they bank. They can tap their phone and transfer money or even log in and get a loan on their phone. In so many ways, banking is faster and more immediate than ever.

As Chris Skinner, author of Digital Bank, puts it, “We built an industry on the physical distribution of paper in a localized world, and we’re now having to get to grips with the digital distribution of data in a networked world.” For bankers, it’s not business as usual.

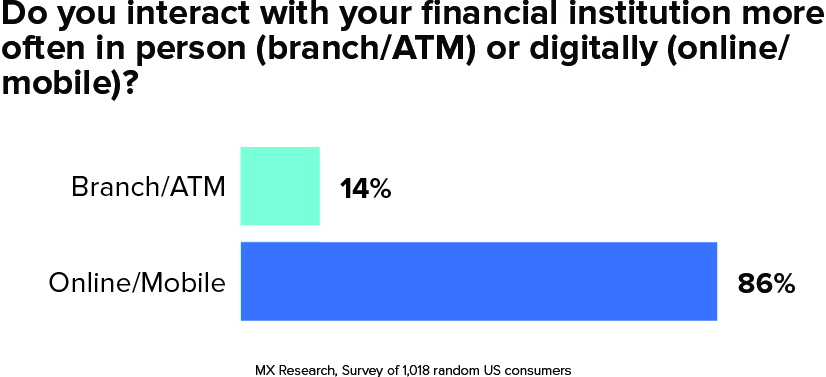

We saw this shift reflected in an original survey we ran with random US consumers, cited throughout this ultimate guide. For instance, when we asked which channels they interact with most often, the vast majority of respondents (86%) said digital channels.

What does this mean for you?

If you’re in financial services, it means you have to evolve, to transform your institution top to bottom into a digital company.

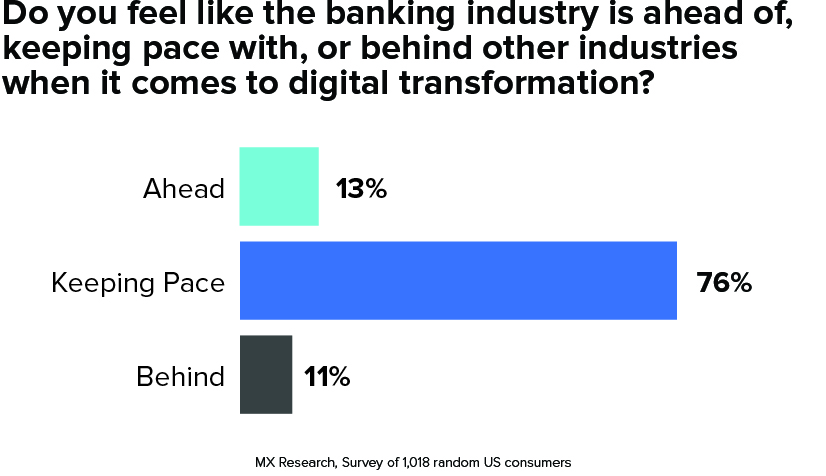

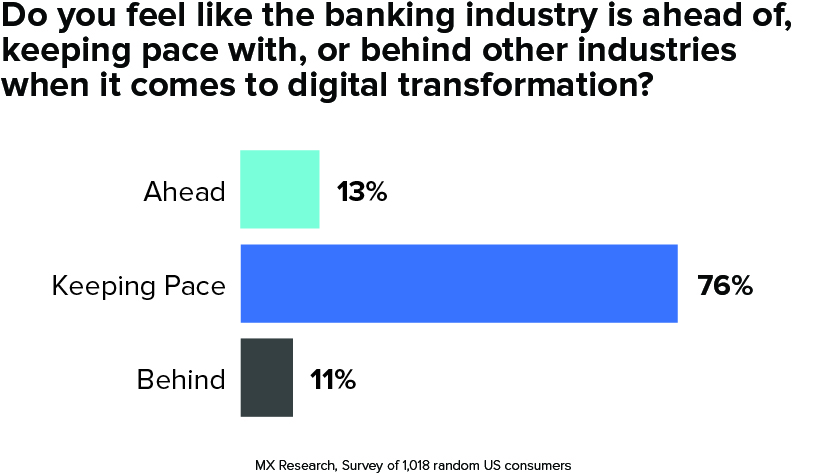

Fortunately, this isn’t a message of doom and gloom. To the contrary, we want to note at the outset what’s going right. For instance, 76% of consumers say that they feel like banking is keeping pace with other industries when it comes to digital transformation, and only 11% say they feel it’s behind pace. In light of this, the message is largely one of saying, “Stay the course — and make sure you’re one of the institutions thought of as keeping pace or getting ahead.”

And yet, this survey response might paper over some of the problems you’re facing. You might ask yourself, for instance, how your institution fares on this front. Are you ahead of, keeping pace with, or behind the most advanced companies in financial services?

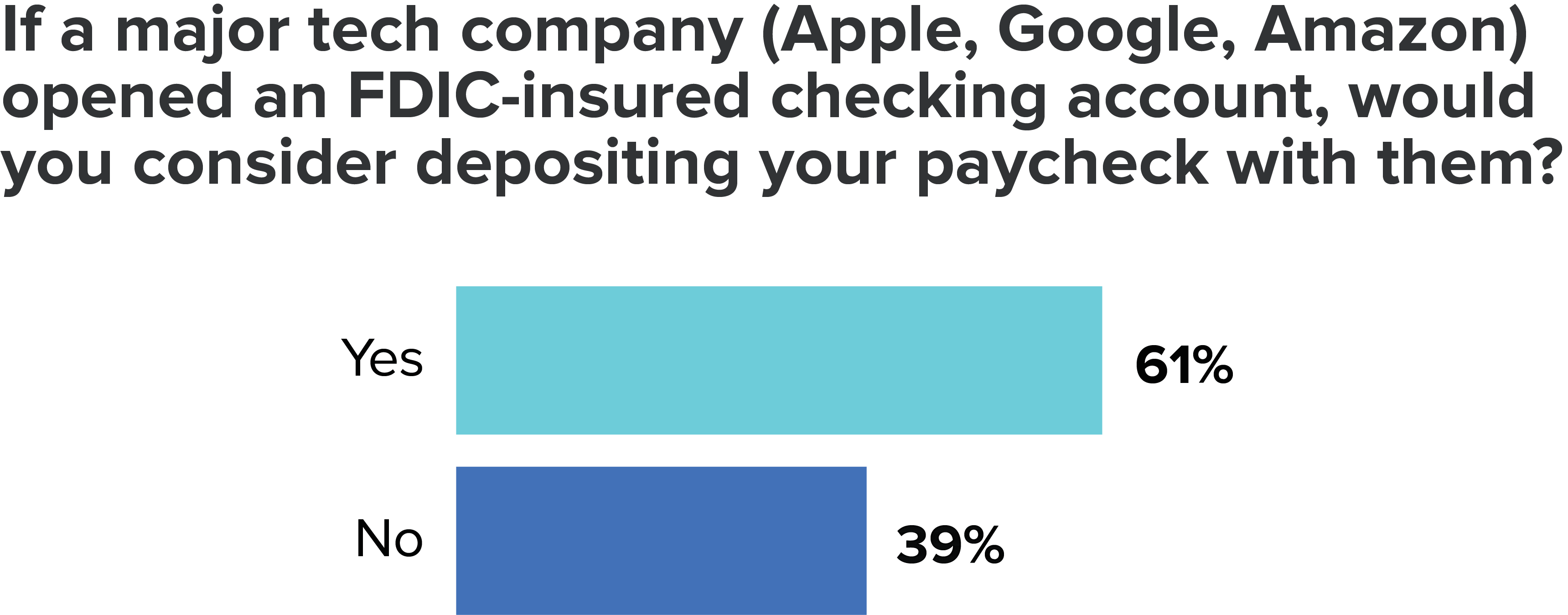

In addition, are you prepared for the possibility of new entrants in the space? Apple is expanding their reach into payments and PayPal is offering business loans up to $500,000. And consumers say they’re open to these new entrants. For instance, 59% of US consumers say they’d consider applying for a loan at a major tech company in the event these companies offered a loan that met their needs.

And 59% said the same thing about using a major tech company to deposit money.

None of this necessarily means that these tech giants will become banks. But it does mean that if these tech giants partnered with a bank (as Apple did with Goldman Sachs for Apple Card), a majority of consumers would consider using their tech. Think of how easy it is to adapt Apple Card. Users sign into their wallet app on their iPhone, click Apply, fill in their info (much of which is auto-populated), and click Accept. It’s so convenient and simple that users are going to have a hard time accepting prior methods.

Apple: Setting the standard for simple onboarding

It’s not hard to see why simplicity matters. People check out mobile app ratings and talk about mobile banking options with their friends. Then they choose a best-in-class option. For many people the mobile banking experience is their banking experience.

Or think of how easy it is to send money via Venmo. Users open the app, find the username of the person they want to send money to, and send the amount they want to send.

If you don’t offer experiences that are as simple as this, you may find that upcoming generations will have little time for you. The truth is that banking is no longer about having the primary presence in a local community. It’s about delighting users via digital technology.

How do you make this transformation?

That’s where this guide comes in. By reading this guide, you’ll establish yourself as someone who knows what’s essential about digital banking and what’s not. You’ll get a sense of what you can do to help your financial institution thrive in the coming decades. Best of all, you’ll realize that you don’t have to do it all alone. Finding the right fintech partner will help you see that the transition to digital doesn’t have to be overwhelming. You can get guidance at every step along the way to becoming a leader in digital banking.

Start With Advocacy

Given the increased choice and decreased friction the banking industry faces, it’s imperative to do what’s right for the end user. “If you're not consumer obsessed,” says Ryan Caldwell, CEO at MX, “I don't know that you can really survive in this new world.” It might not happen overnight, but as it becomes easier and easier to open a new account, consumers will be less and less accepting of companies that don’t have their best interests in mind.

To succeed in the transformation to digital, then, you have to start with a deep commitment to advocacy. You have to do what’s right by the user.

Industry Highlight: USAA

In many ways, USAA sets the standard on this front with their mission “to facilitate the financial security of its members, associates and their families by providing a full range of highly competitive financial products and services.” Neff Hudson, Vice President of Corporate Development at USAA, says "The question that you have to answer at USAA is, ‘What are you doing for the member?’ If you can't answer that question, your project is probably not going to get across the finish line." For Neff, the focus is around building “autonomous finance” — financial guidance powered by clean data and artificial intelligence. “We're going to be able to invent autonomous finance as an industry,” he says, “but it had better be invented with the customer in mind. If it's invented to make the balance sheet look good, I don't think we're going to like the results in the market.” As in so much else, USAA’s drives what they do.

Starting with advocacy means that, above all, you work to empower people to be financially strong. You focus relentlessly on long-term gains — not on short-term wins. If something takes advantage of a user, making their lives more miserable in the long run, you don’t do it. Instead, you do what’s right by your users. You recognize that without deep user loyalty, you won’t be able to thrive in the digital age.

With this mission firmly in place, you’re ready to work toward a true digital transformation.

To do it right, follow these three steps:

- Build on a foundation of data.

- Give users the best digital experiences.

- Focus on growth.

A strong foundation of advocacy is built on a strong foundation of data and experience, leading to growth.

3 Steps to Digital Transformation

Build on a foundation of data.

It All Starts With Data

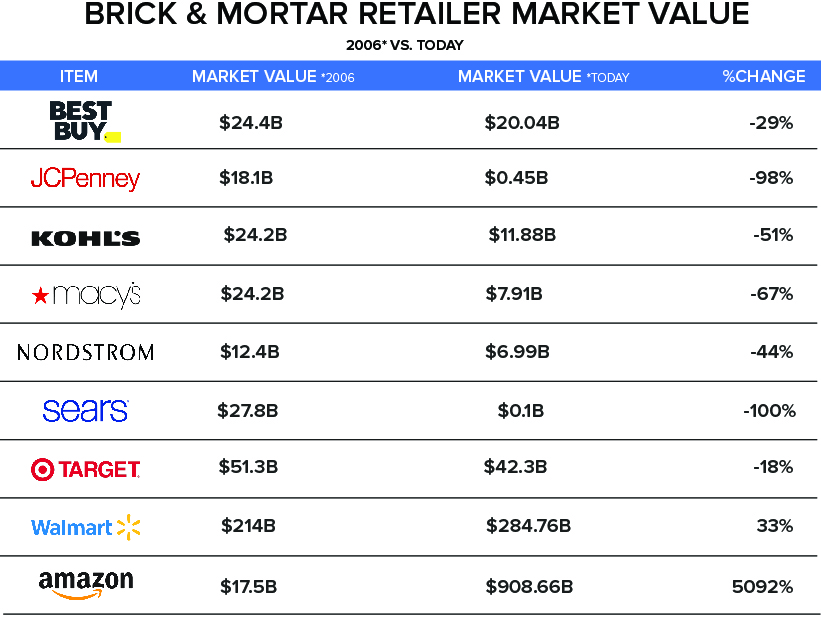

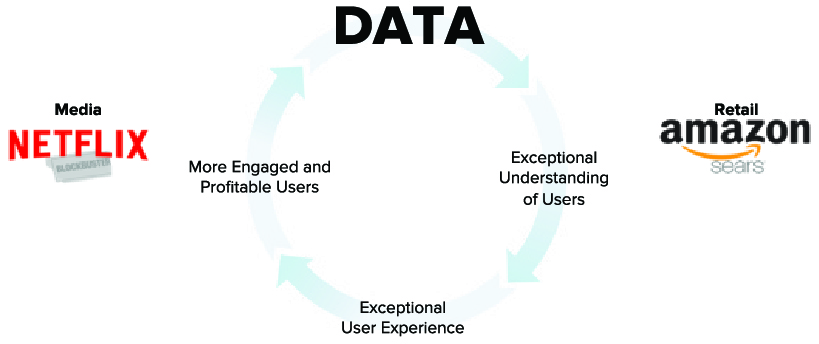

Data-enabled disruption has overtaken key industries again and again, perhaps most famously when Netflix and Amazon overpowered competitors from Blockbuster to Sears.

While the primary benefit Amazon provides is an effortless, one-click experience where products show up on your doorstep two days after purchasing them, data powers everything behind the scenes.

It works like this: The more engaged users that Amazon has, the more user data they acquire. This data helps them offer a more compelling experience to these users (and promote their own products), which in turn drives up the number of profitable users. The whole cycle is a flywheel that spins faster and faster with each turn, widening the gap between Amazon and their competitors.

Financial institutions can and should leverage this same data flywheel effect. After all, they collectively capture trillions of data points, creating a goldmine of essential insights on end users.

To do it well, focus on data aggregation, data enhancement, data analytics, and data discovery.

Data Aggregation

Aggregation enables users to see all their accounts and transactions in one place. For example, if ACME Financial offers account aggregation, users can log in and view data from potentially anywhere they have a financial account — all through ACME Financial banking portal. In short, aggregation turns ACME Financial into a one-stop financial hub.

The process generally requires either “scraping” a financial institution’s website by mimicking human behavior or connecting directly through a data exchange. Of the two, connecting via a data exchange is a vastly better experience since it’s the fastest and most secure way to aggregate financial account.

However it happens, data aggregation empowers both the end user and the financial institution. The end user sees all their finances in one place, and the financial institution gathers all the data it needs to best help their end users.

Data Enhancement

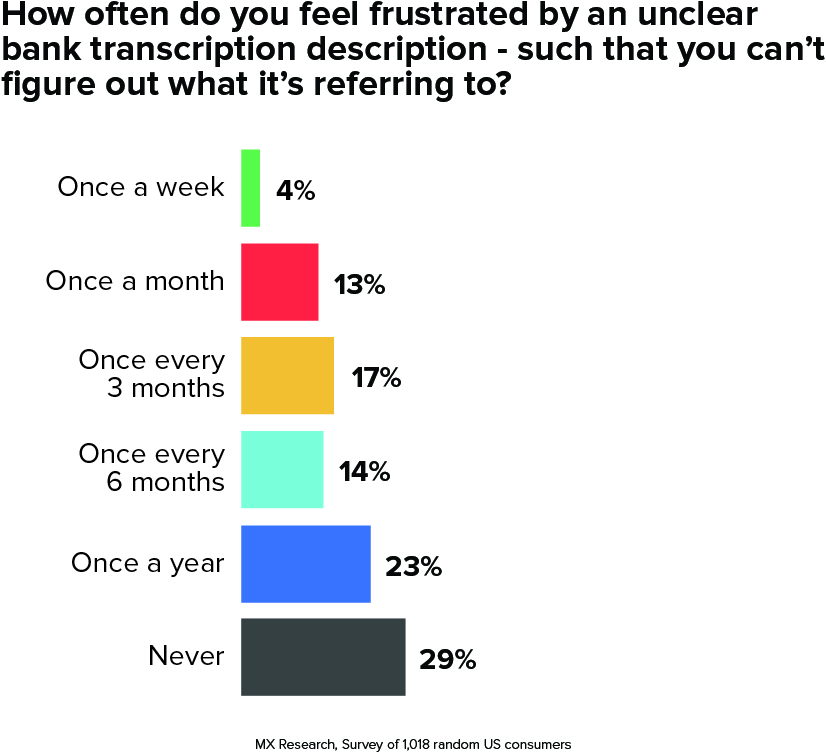

Of course, it’s not enough to just aggregate data — largely because raw transaction data is often totally incomprehensible. Who knows what a transaction description like CSI-308613/22120-CHV refers to?

The fact is that consumers feel frustrated with unclear transcription descriptions, with 71% of consumers saying it happens at least yearly and 17% saying it happens at least once a month.

This results in user frustration, complaints to your call center, and a negative perception of your brand. In addition, it does little to help you understand your account holders. How can you make use of the data to empower people to be financially strong if the data isn’t clean?

If you’re going to fix this problem, you’ll want transaction data that has been cleansed, categorized, and classified.

Cleanse. When your users can’t understand a transaction description, they don’t get upset with the vendor or the card provider. They get upset with you. They dial in to your call center and drain your employee’s time. You can prevent this problem by cleaning all descriptions.

Categorize. Your users are looking for help with their finances, and they don’t want to spend all their time tracking their spending habits. By adding automatic categorization to your transaction feeds, you help these account holders better manage their money while improving user loyalty, driving revenue growth, and paving the way for future technology.

Classify. When you properly classify transactions, you can see which of your users’ transactions are marked as bill pay, direct deposit, fees, and more — giving you the ability to more precisely target end users. For instance, you might target account holders who use bill pay with your competitors to use bill pay with you instead (amping up your bottom line).

Enhancing transactions this way — through cleansing, categorizing, and classifying — sets the right foundation for not only a better mobile experience but also for whatever the future may bring. For instance, if you want to offer voice-assistance or AI-enabled features, you need clean data. (These features are useless without it.) As Ron Shevlin, Managing Director of Fintech Research at Cornerstone Advisors, asks, “If you don't have good data and analytics capabilities, what good will an AI-first strategy do?” You have to lay the right foundation with data before you start dreaming of an advanced user experience.

Data Analytics

Do you know how many of your account holders use your digital products at least weekly? Do you know how many have aggregated an external account? Or what percentage have a loan with you?

If you have this information, is it easily accessible — or is it buried in a database that’s difficult to view?

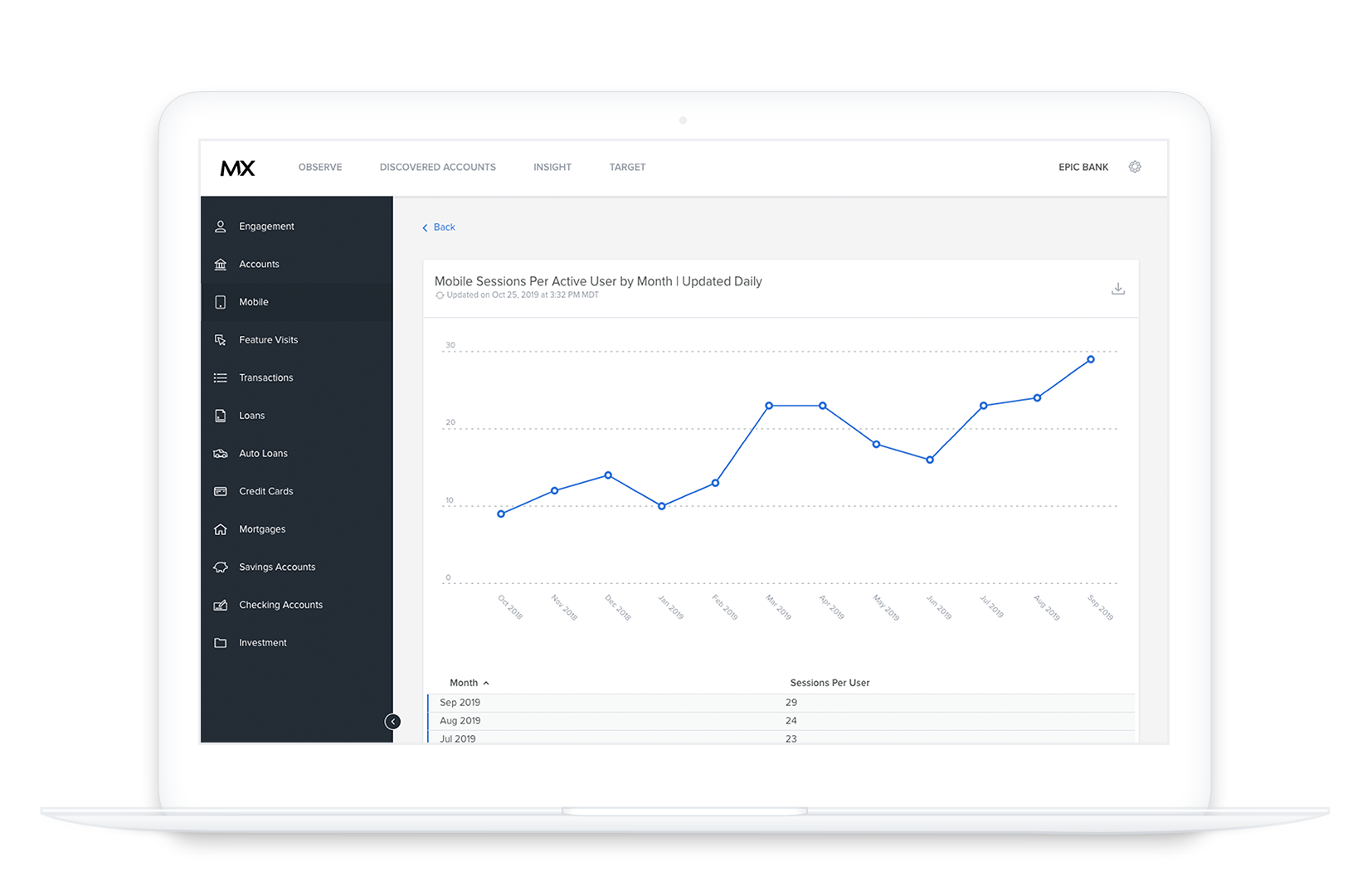

To transform into the digital era, you’ll want all essential data to be instantly available via a realtime dashboard.

This might include:

-

Engagement Data

- Total users over time

- Users with aggregated accounts

- Accounts per user

-

Account Data

- Total accounts

- External accounts per user

- Accounts by type

-

Mobile Data

- Total mobile users over time

- Mobile sessions per active user by month

- Active mobile users by OS

-

Mortgage Data

- Total users with mortgages

- Mortgages by organization

- Mortgages by interest rate

-

Credit Card Data

- Total users with credit cards

- Credit card balance by organization

- Credit cards by coarse interest rate

-

Investment Data

- Users with investments

- Investment balance by organization

- External investment accounts by organization

...and much more.

Again, the point isn’t just to have this data in a database somewhere in the organization. The point is to have it on hand and ready to make use of.

Data Discovery

Once you have a 360-degree view of each user’s data, have cleansed, categorized, and classified it, and have it all available via a dynamic dashboard, you’re set to make discoveries about your client base.

Among many things, you can learn how and when money leaves your institution to a competitor’s institution via a myriad of transaction types (including credit card and loan payments). This process, known as Discovered Accounts, sets your financial institution up to target these users with a personalized offer that directly undercuts your competitor, encouraging the end user to switch their full loyalty to your bank or credit union.

For instance, one major US bank ran a deep analysis on their users’ total card payments and found that $1.6 billion of their users’ money was going toward cards at other competing companies. This discovery enabled the bank to be more methodical about deepening their relationships with their clients.

It All Hinges on Trust

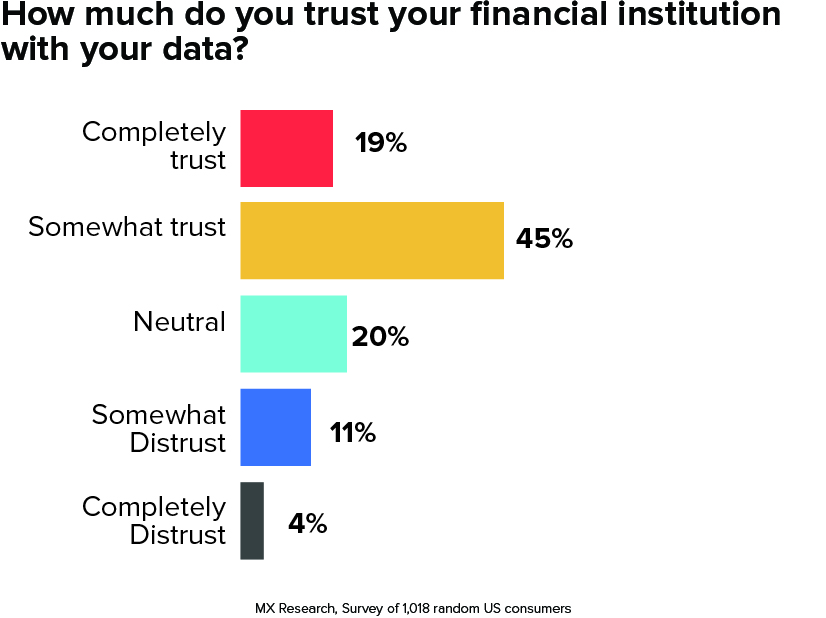

When we asked US consumers how much they trust their financial institution with their data, we found that only 19% said they have complete trust.

Fortunately, the news isn’t all bad for banks and credit unions. After all, only 4% said they completely distrust financial institutions with their data.

However, these numbers do indicate that there’s room to improve.

It’s true: The move to advanced analytics is a difficult hurdle to overcome. However, banks and credit unions that start turning the flywheel now will win the gains that come with momentum. The more they make use of the available data, the better they will be able to personalize their services to their audience. In the process, they’ll win more users and get more data, which in turn will improve the user experience.

Give users the best digital experience on the market.

A study from Virtusa found that the number one priority at financial institutions is to improve the digital customer experience. As Brett King, author of Bank 4.0, says, “Banking is being redesigned to fit in a world where technology is pervasive and ubiquitous; the only way you stay relevant in this world is by creating experiences purpose-built for that world.”

Whether we’re talking about online banking or mobile banking, the principles are the same. You’ve got to offer a digital experience that at least is keeping up with digital offerings. Fortunately, as we covered above, most people believe that on the whole the banking industry is keeping up on this front.

However, it’s not enough to produce something that keeps pace — particularly when it comes to mobile banking. You have to edge out your direct competitors. Why? Because nearly 70% of people say that they only have one to three financial apps on their phone.

If you’re not in the list of the one to three financial apps people use, you may be missing out on the mobile relationship with your users.

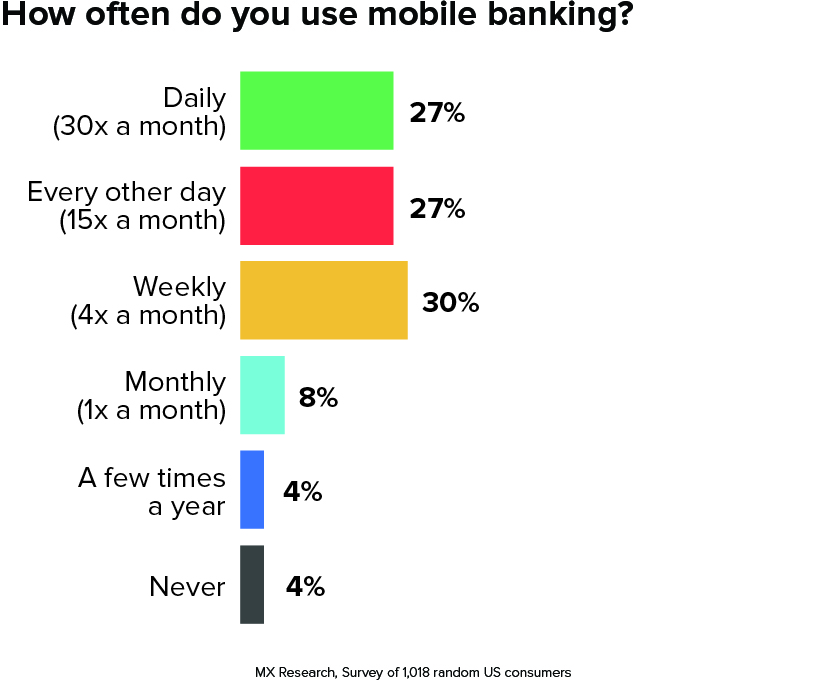

It’s not hyperbole to say that your success might completely hinge on getting this right. After all, we’ve found that 84% of consumers use their mobile banking app at least weekly and 26% use it daily.

If your competitors own this relation instead of you, the chances of you being considered your users’ primary financial institution are nil.

So, how do you create an optimal digital experience?

As we cover in depth in our Ultimate Guide to Mobile Banking, the answer requires you to follow ten essential principles:

-

Start with why. Build with a clear understanding of what’s motivating you to offer the right digital experience. If you’re building with the right cause in mind — to empower the world to be financially strong — your team with have the tenacity to stick with the project when things get difficult.

-

Make it secure. When we asked consumers what makes them hesitant to use mobile banking, 56% said they have no hesitancies. However, 31% cited security as their top concern. To address these concerns, adopt a defense-in-depth security model, maintain all protocols (including SOC-2 Type II Report and PCI DSS), and make sure your users know everything you’re doing to keep their data safe.

-

Build on a cross-platform framework. Whether it’s online banking or mobile banking, people want a cohesive digital experience. One of the best ways to do this — and excuse our tech-speak here — is to build a foundation of C++ and use a software developer kit (SDK) to code up to each device type.

-

Listen to your users. The more you listen to your users, the better you’ll be able to meet and exceed their needs. To do this, hold regular usability tests, provide users with a way to voice their opinions, and proactively ask for feedback.

-

Innovate in weeks, not years. Once you’ve adequately listened to your users, you’ll want to integrate their suggestions. Otherwise, what’s the point? Unfortunately too many efforts in digital banking take far too long to integrate. You’ll want a method that allows you to adapt quickly.

-

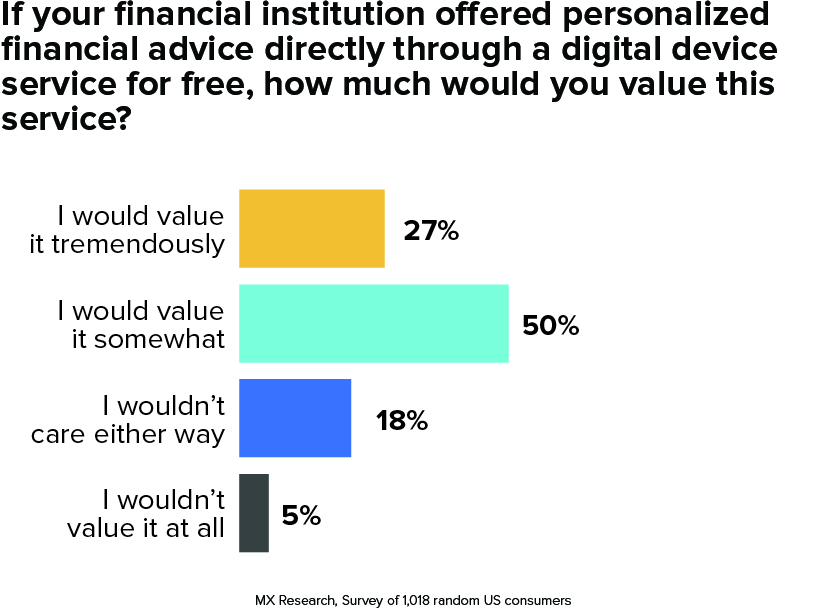

Enhance your transaction data. One of the main purposes of enhancing data is that it sets you up to personalized financial advice, a service that 77% of consumers say they would value.

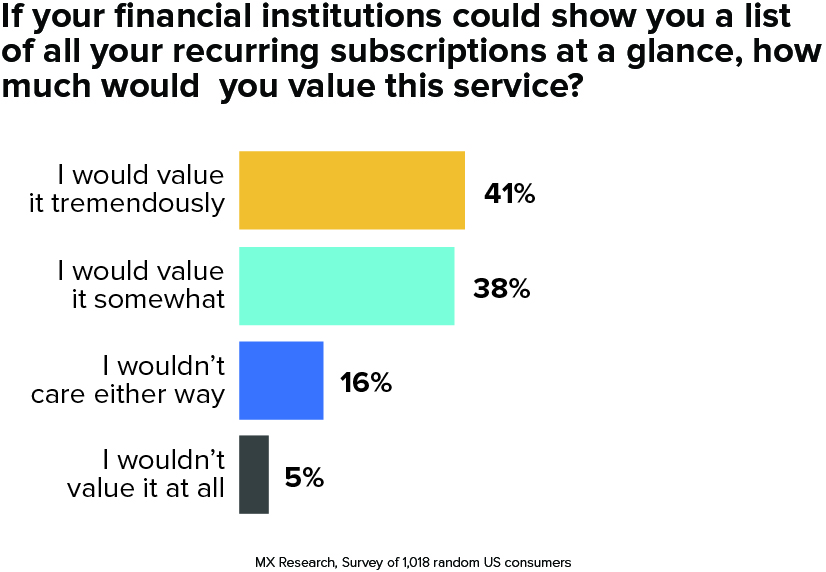

The same could be said of offering a more specific service such as flagging a user’s subscriptions so they know at a glance what they’re paying for each month. Nearly 80% of consumers said they would value such a service, with 41% saying they would value it tremendously.

-

Offer a full range of features. These features include digital account origination, biometric sign-in options, external account aggregation, money management, money transfers, fraud alerts, notifications, in-app tutorials, in-app support, remote deposit capture, credit score information, and more.

-

Offer a personalized experience to differentiate your brand. People use digital banking for a variety of reasons. Because of this, they’re looking for ways to make the experience their own. For instance, if someone primarily wants to see their latest transactions, they should have the ability to put that information at the top of their digital experience. Customization driven by the user is key.

-

Choose partners you can innovate with. When it comes to digital, the name of the game is partnership. The fact is that no single company can do everything on their own. To get the most out of each partnership, you have to ensure that your partners share your innovative spirit — or even push you to be more innovative than you may be comfortable with.

-

Build for the future of banking. Whether it’s digital watches, voice-enabled devices, smart fridges, smart thermometers, virtual reality, emotional trackers, or something humans haven’t imagined yet, you’ll want to be ready now instead of having to catch up each time a new technology comes out.

If you follow these ten principles, you will be well on your way to offering the best digital experience on the market. In addition, you can leverage the power of MX Enabled, a single integration point for banks, credit unions, and fintechs to collaboratively innovate.

Enjoy transformative growth.

If you work in financial services, you want to grow relationships and trust.

But how do you do that in the digital age? As we’ve covered so far, you have to take your strengths — the networks you’ve established, the skills you’ve developed, the experience you’ve accumulated — and build on a foundation of data and experiences.

Once you’ve laid this foundation, you’re ready to quickly grow. You’re reaping the benefits of the data flywheel effect and you’re giving users their primary digital experience.

Now you can direct them to do what’s in their best interest and build long-term loyalty in the process.

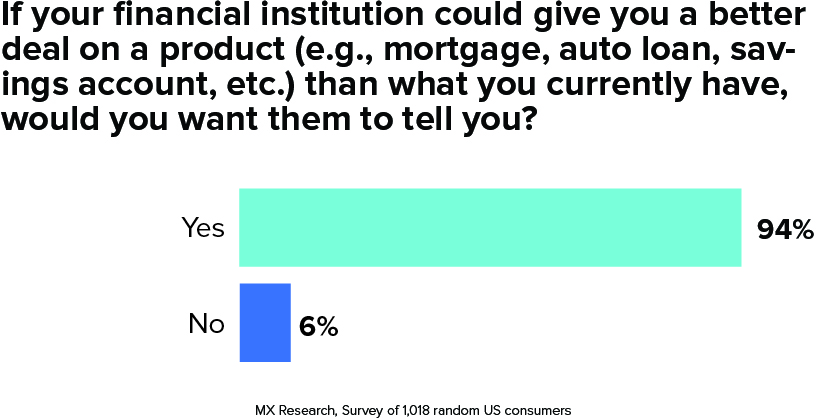

After all, it’s exactly what consumers want. They want to know that you have their best interests in mind — that you’re using their data to help them. For instance, 94% of respondents say that if their financial institution could offer a better deal on a product they currently have, they would want to know.

Can you build a personalized message for each user depending on their particular financial situation? You can if you’ve built on a foundation of data, if you’ve engaged them via digital channels, and if you have the capacity to act on both those fronts.

By gathering a 360-degree view of your users’ financial dashboard, you will see every time they have a product with a competitor, and you will be able to undercut that offer to win their business.

If you aren’t doing this, you should know that your competitors might be. In either case, this is a critical approach to growth in the digital age of banking.

Innovate with Digital Onboarding

Once you have established your institution as the go-to source for digital transformation for your current account holders, the final step is to go full throttle with growing your user base by appealing to new consumers.

Traditionally, this has meant pouring money into traditional marketing efforts: billboards, flyers, mailers, community events, etc. But the opportunities for onboarding new users expand in the digital age.

For example, with external account aggregation, you don’t have to limit your mobile banking app to people who have an account with you. After all, anyone could download your app, add their accounts, and manage their money via your app. This puts you in the position to own the mobile relationship with these consumers, which will become more essential as time goes on. After all, nearly 70% of consumers say they only have 1-3 finance apps on their phone. If yours isn’t one of them, how do you expect to become their primary financial institution?

The process works like this. You find a target audience you want to appeal to, and offer them an incentive to download your app. Maybe you run targeted social media ads, letting people in your community know that you have a new money management app that works regardless of whether they have an account with you. Or maybe you run a promotion at an event — say a sporting event or a movie in a theater — where you offer to cover the cost of concessions if they download the app and connect an account. Once you have one account aggregated, you can transfer money to them, give them pointers on how to use the app, and (most importantly) use that data to show them that you can give them a better financial product than the one they currently have with the account they aggregated.

It’s the perfect way to build a relationship with non-account holders in the digital age since it’s a digital onboarding process. No need for them to come in to sign a physical piece of paper. No need for them to meet anyone face to face. They just download the app and add an account. And since you can offer them a way to create an account with you directly in the app itself, it’s the perfect step for them to start thinking of you as their primary financial institution — particularly because the next time they’re looking for a loan, you’ll be able to message them directly in the app they use daily to manage their money.

Conclusion: Empower the World to Be Financially Strong

Given the increased choice and decreased friction in the digital age, the goal of all financial services companies must be to do what’s in the best interest of the end user by empowering them to be financially strong. Put simply, that’s the best way to win their long-term loyalty. (Otherwise, they’ll bank elsewhere.)

Transformational growth starts with transformational experiences, transformational experiences start with transformational data, and transformational data starts with MX. While the process can feel overwhelming, know that you don’t have to do it alone. Partners like MX can guide you every step of the way so you can confidently make the transition to digital.

About MX

MX empowers the world to be financially strong by helping to create a financial services industry that’s optimized for the digital age. That’s why we partner and guide banks and credit unions toward growth, experiences, and a foundation of clean data. MX will be your partner and guide as banking transitions to digital.

The Ultimate Guide to Digital Transformation in Banking

The Ultimate Guide to Digital Transformation in Banking