If you’ve worked in financial services for any amount of time, you know that data matters. What too often goes unsaid, however, is precisely why data matters, how to create a culture that uses data effectively, and what data solutions you should consider to actually bring results.

Since MX is a fintech company, you might expect us to tell you that you should immediately implement our cutting-edge technology to get ahead of the competition. In reality, our position is just the opposite. We believe that you shouldn’t start with technology and that you should instead start with an adaptive culture, which emphasizes the need to effectively prepare your organization to effectively use new technology. After all, what good does technology — even the best technology — do if no one uses it? It’s far better, in our opinion, to lay the right cultural foundation before you ever consider what technology you want to use (whether it’s ours or our competitors).

With this in mind, this ultimate guide will focus almost entirely on why data matters and how you can change your culture — all for the purpose of increasing market share and profitability.

As part of our ongoing research on this topic, we surveyed more than 1,000 employees in financial services to learn how their organizations rank on a range of measures, including their data strategy. We pull from this survey and other research for this guide.

We’ll first look at why data matters and then move into how to get there.

Why Data Matters

Build a Sense of Urgency

Achieving the promised results of a successful data transformation hinges almost entirely on whether your team believes the process is urgent. If the thought of transformation induces yawns across your team, that’s a nonstarter. You won’t have luck with datatech adoption. Another critical dependency is commitment to a successful digital transformation must originate from the top of the house. When the top leaders in the organization, even up to the CEO “owns” and are committed to succeeding, decisions related to digital transformation are not deprioritized as easily when the pressure of daily work inevitably comes into conflict.

So, how do you build urgency? Start with this primary question:

What key advantages does data optimization give our competitors?

Here are a few advantages to consider.

The Primary Financial Hub

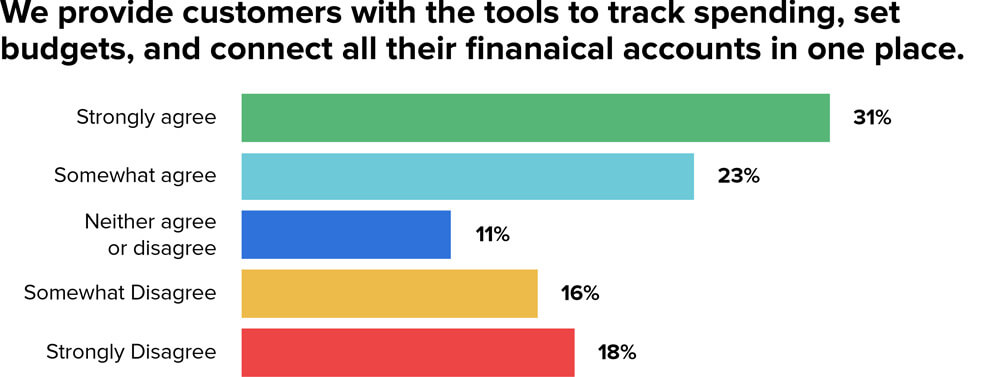

Our original survey of 1,000+ employees in financial services revealed that 54% say they either strongly agree (31%) or somewhat agree (23%) that they currently provide customers with the tools to track spending, set budgets, and connect all their financial accounts in one place.

MX Research, Survey of 1,000+ Employees in Financial Services

At first glance, this might not seem like a big deal to the remaining 46%, who might think this data points to the personal financial management products of yesterday. However, what these laggards might not realize is that enabling customers to connect all their accounts in one place sets a company up to be the primary financial hub for their users.

Additionally, thanks to the acceleration of technology and the fact that UX standards are set by other industries, customers expect these services and tools from their financial institution. Personal financial management tools are now considered “table stakes” much like debit cards or online banking services.

If you’re not the primary financial hub, your competitors will be. This means that your customers will sign into your competitors’ apps instead of yours, and you won’t be on the home screen of your customers’ smartphones. Once you lose that position, your relationship with those customers could hang by a thread. After all, your customers can get the information you provide them in your competitors app and therefore no longer need to sign into yours. They will see your competitor’s in-app messaging, not yours. They will think of your competitor for all new financial products. And when that competitor offers them a better deal, they might take it and forget about you altogether.

The truth is that if your customers can only view the accounts they have with you in your app, they’ll never consider you their primary financial hub. Why? By definition, being the financial hub for your customers requires them to see all their data in one place.

Customer Insights

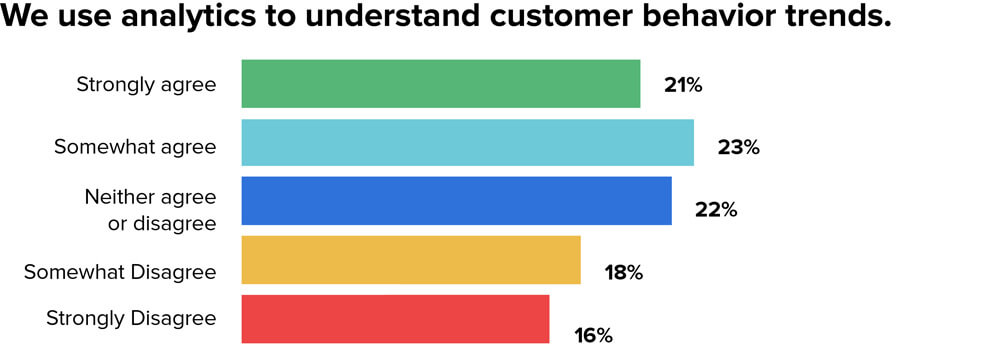

When customers add all their financial accounts in your competitors’ app, they have their complete financial picture, including data about the accounts those customers also have with you. This is the simplest way to truly know the financial lives of customers and get a sense for their user base.

A slight minority of financial institutions in our survey say that they have this ability, with 21% saying they strongly agree and 23% saying they slightly agree.

MX Research, Survey of 1,000+ Employees in Financial Services

This means that there’s still some room to lead out here if you’re not already. It also means that plenty of institutions are already perfecting their ability to know their customers and then create better products for those customers (which in turn creates more customers). This is known as the data flywheel effect, and it has quickly set apart companies like Amazon as they leverage their data to better serve users in a cycle of engagement. The flywheel spins faster and faster as data and engagement feed off each other – all while Amazon’s lead against the competition gets wider and wider. The same is true of financial companies that are implementing the data flywheel effect today.

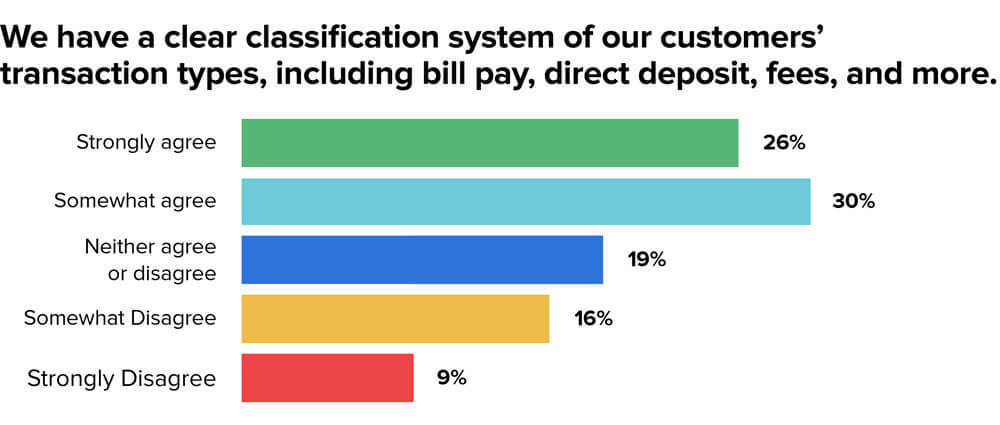

To enjoy the benefits of the data flywheel effect, it helps to gather a range of data. A majority of respondents (56%) said they either strongly agree (26%) or somewhat agree (30%) that they have a clear classification system of their customers’ transaction types, including bill pay, direct deposit, fees, and more.

MX Research, Survey of 1,000+ Employees in Financial Services

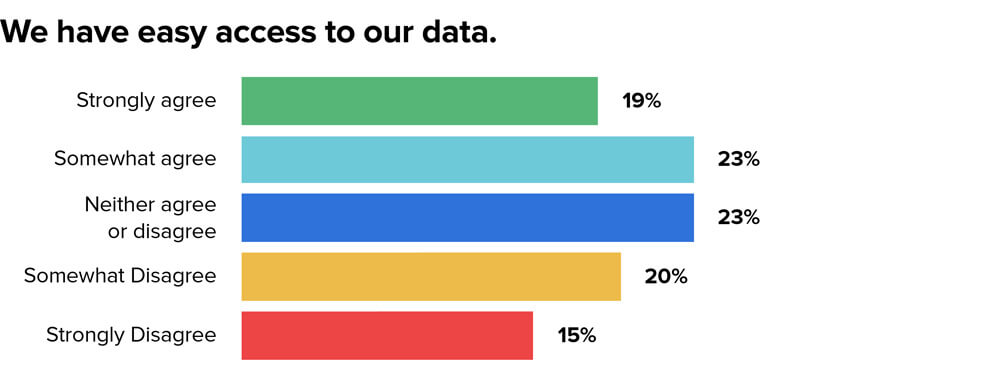

Finally, there’s the matter of having easy access to data, which makes pinpointing customer insights viable. Less than half of respondents said they either strongly agree (18%) or somewhat agree (23%) that they have easy access — signifying an area where financial institutions could use a lot of support.

MX Research, Survey of 1,000+ Employees in Financial Services

Hyperpersonalized offers

Competitors that have a solid database at hand are well equipped to make hyper-personalized offers — offers built for the exact individual who sees them. In our Ultimate Guide to the Future of Banking, we found that 94% of consumers say that if their financial app could offer them a better deal on a product (e.g., mortgage, auto loan) than they currently have, they would want to know.

Ask yourself how you’re doing on this front. Can you see whether a customer’s mortgage rate with your competitor is too high? Can you see whether they’re paying too much for a car loan? The right foundation of data gives you the ability to use this data to make hyper-personalized offers, win business directly from your competitors, and positively impact the lives of your customers. Those who don’t have this ability will find they’re on the losing end of this situation.

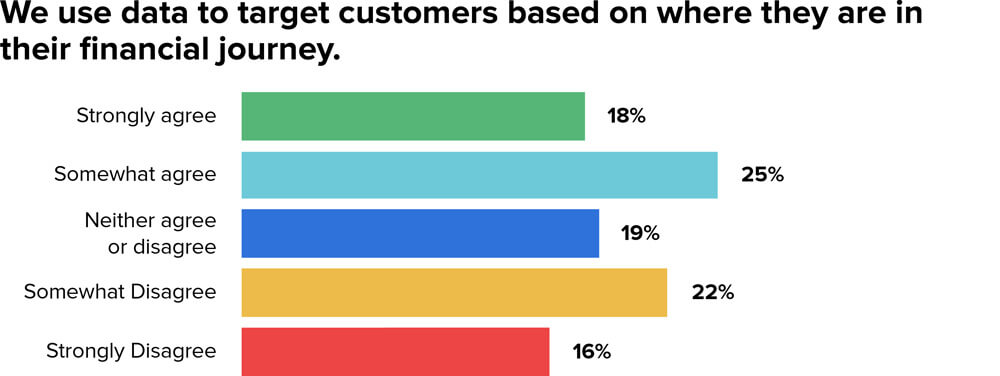

There’s room to stand out here, as only 18% of respondents in our banking diagnostic survey said they strongly agree that they use data to target customers based on where they are in their financial journey.

MX Research, Survey of 1,000+ Employees in Financial Services

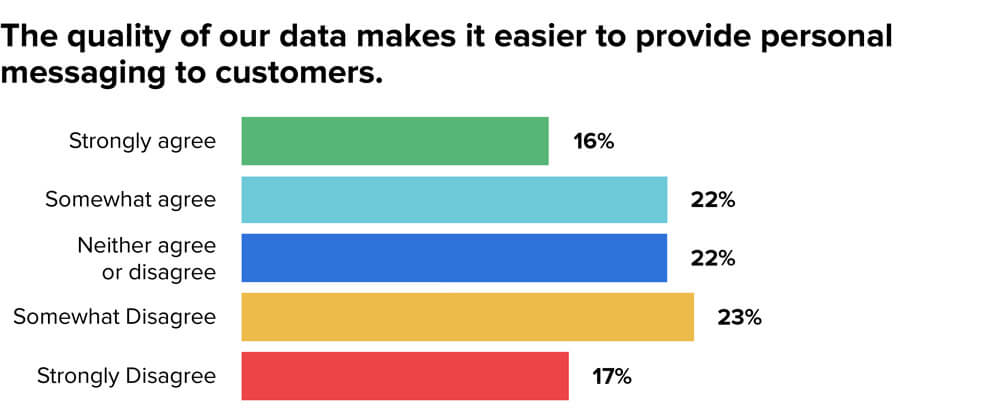

And only 16% of respondents said that they strongly agree that the quality of their data makes it easier to provide personal messaging to customers.

MX Research, Survey of 1,000+ Employees in Financial Services

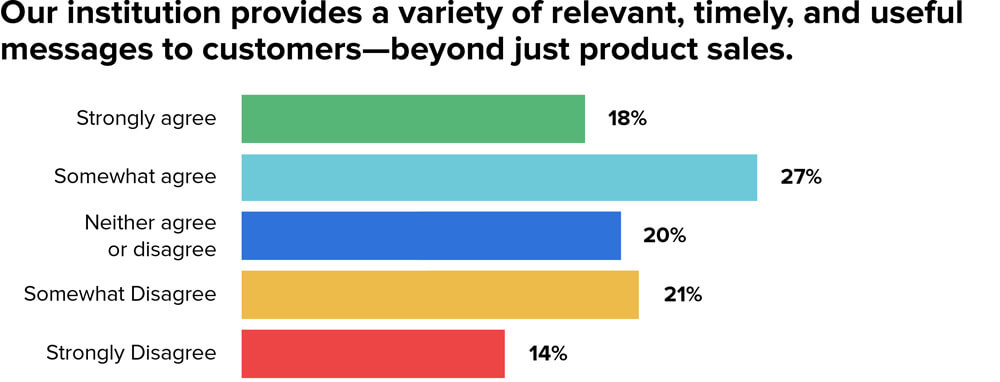

Similarly, only 18% said they strongly agreed that they provide a variety of relevant, timely, and useful messages to customers beyond just product sales.

MX Research, Survey of 1,000+ Employees in Financial Services

If your direct competitors count themselves among the institutions that offer hyper-personalized offers based on a 360-degree financial view, you can guarantee that they’re using your data — accessed via account aggregation — to make those offers. By harmonizing your data, you can outsmart your competitors.

Real-time financial guidance

According to a study from J.D. Power, 78% consumers are interested in “receiving financial advice or guidance from their bank,” but only 28% say they feel they get such advice. More specifically, 58% of consumers say they’d like their financial institution to give them advice via web and mobile, but only 12% say they get advice this way. Paul McAdam, J.D. Power senior director of the banking practice, says, “The key takeaway from this study is that there is a huge opportunity to leverage a combination of in-person and digital interactions to provide advice and guidance that assist customers in their financial journey.” He adds, “The industry’s service improvements have led more customers, particularly younger ones, to view their retail bank as a viable provider of advice.”

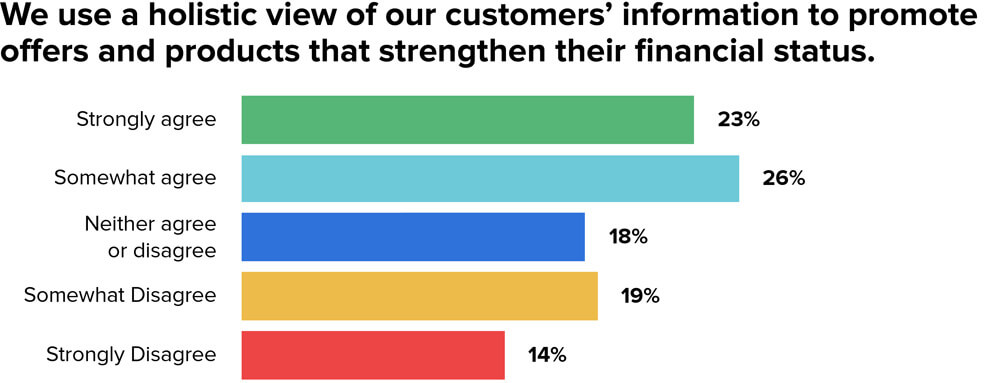

With only 12% of consumers saying they feel like they get financial advice from their bank, it’s somewhat surprising to see nearly 50% of bankers in our diagnostic survey say that they feel like they use a holistic view of their customers’ information to promote offers and products that strengthen customers’ financial status.

MX Research, Survey of 1,000+ Employees in Financial Services

This represents an enormous disconnect between the views of bankers and consumers, with half of bankers saying they help customers strengthen their financial status and only a portion of consumers saying the same. Herein lies one of the most fundamental shifts that must occur for a financial services company to begin separating themselves from the rest of the pack. It works like this: When you put the best interests of your customers ahead of the (perceived) best interest of the company, the entirety of the customer experience model shifts. You adapt your services, products, and technology to serve the real financial needs of your customers, resulting in an increase in loyalty, share of wallet, and of course revenue. By contrast, a blind emphasis on revenue first will result in disengaged customers who will seek out a company that will put them first.

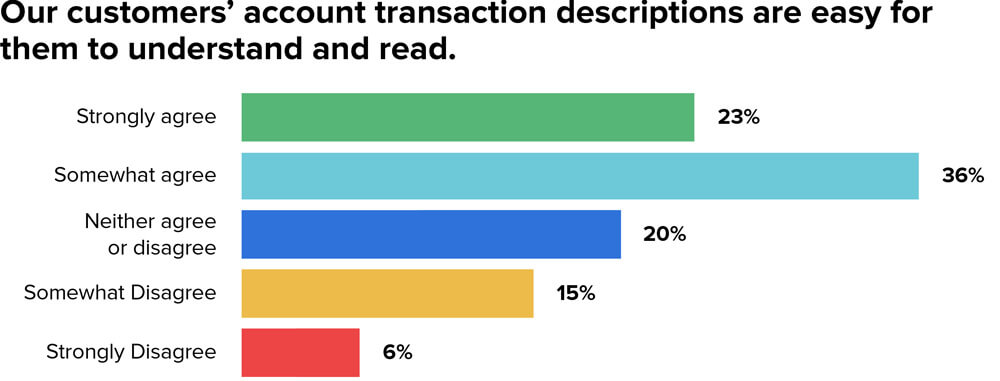

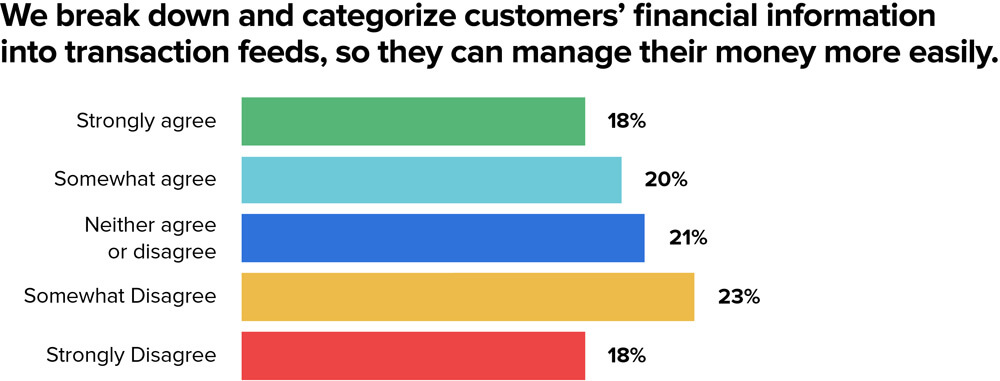

When it comes to helping customers via digital means, the disconnect is even wider, with 59% of bankers saying their account transaction descriptions are easy to understand and read and 48% saying they break down and categorize customers’ financial information into transaction feeds so they can manage their money more easily. (This is compared to the 12% of consumers who say they get financial guidance via digital means.)

MX Research, Survey of 1,000+ Employees in Financial Services

MX Research, Survey of 1,000+ Employees in Financial Services

Not being able to provide financial guidance is a deal breaker for many consumers. Annual analysis from Market Force shows that 37% of consumers say that if their financial institutions doesn’t help them improve their financial well being, they see that as a reason to switch providers. If your competitors offer financial guidance and you don’t, these customers might be switching from you to them.

Prepare for the technology of the future

More than anything, a successful data transformation might be the key to setting the scene for the technology of the future. From chatbots to voice-assisted devices to automated money management and a personalized financial news feed, the technology of the future relies on clean, categorized, and augmented data. After all, what good is a chatbot if the data it pulls is incomprehensible to the end user? How can a voice-assisted device serve up useful answers if the data behind it is in shambles? The best way to prepare for the future is to lay a foundation of clean data today.

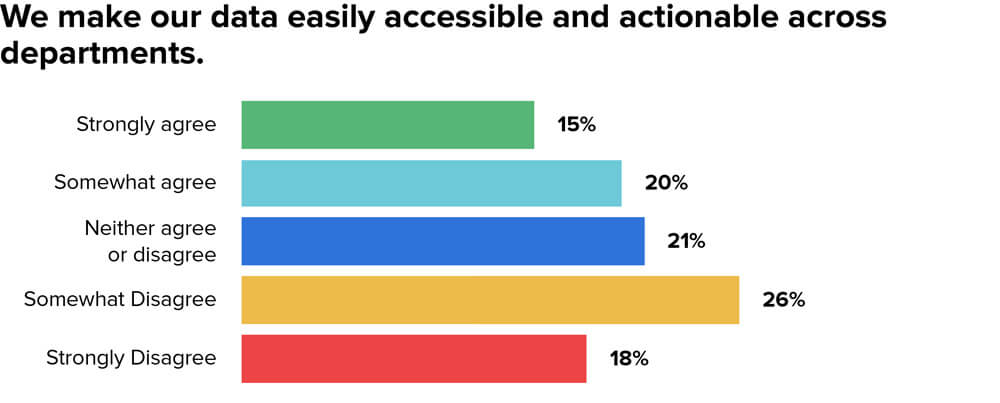

This foundation requires making data easily accessible and actionable across departments, something only 15% of respondents say they strongly agree that they currently implement.

MX Research, Survey of 1,000+ Employees in Financial Services

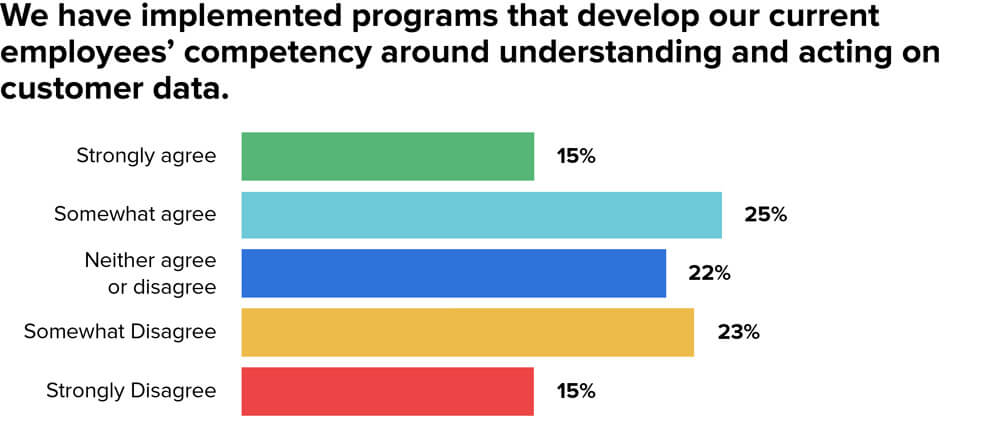

Likewise, only 15% of respondents say they strongly agree that they’ve implemented programs that develop their current employee’s competency around understanding and acting on customer data.

MX Research, Survey of 1,000+ Employees in Financial Services

Taken together, these are signs that most financial institutions haven’t succeeded in laying the right foundation for a successful digital transformation, driven by data. That said, those that have will benefit from the data flywheel as each improvement based on clean and accurate data leads to a better user experience and, in turn, more users.

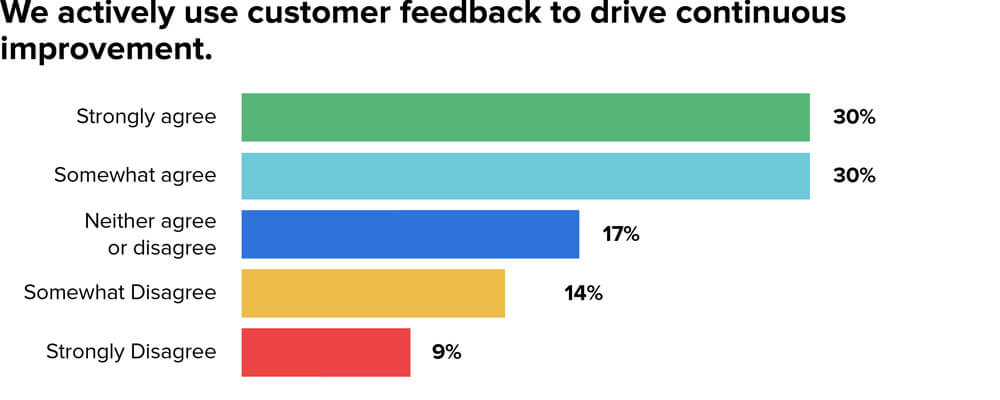

While there is some good news — 30% of respondents say they strongly agree that they use customer feedback to drive continuous improvement and another 30% say they somewhat agree with the same — there is room for making sure that you’re laying the right foundation of data today.

MX Research, Survey of 1,000+ Employees in Financial Services

Why does this matter? Again, it’s all about preparing for the future. As former Federal Reserve official Linda Jeng, says, “If you have access to data, then you have the ingredients to build better services.” And these better services can help optimize customers’ financial lives.

If your competitors outsmart you here, they’ll outsmart you for years to come.

How to Develop a Culture That Uses Data Effectively

Recognize the Challenge Ahead

Too often, people behind large initiatives in financial services fail to recognize that the solution is greater than simply implementing a new technology or tool. Why is this? It’s hard to see that transformation initiatives — particularly data transformation initiatives — are never complete. After all, consumer preferences and behaviors constantly evolve.

If your organization is stuck doing what they’ve always done, they won’t recognize the subtle shifts in consumer expectations. Helping your customer-facing business lines think about how to better understand customers by using data (and then empowering them to take appropriate action to serve those customers) will elevate the loyalty, satisfaction, and trust customers feel towards your organization. This is one of the hardest things any financial services company will experience, which is why it’s important to reiterate that the vision and direction must be owned by the top leadership in the company.

Create a Vision and Communicate It

Once a core group of your team members fully senses the urgency behind getting the right data strategy in play, you’re ready to create and communicate a vision you can share with the entire company to get everyone on board. The goal here isn’t to get 100% agreement on every possible way forward across your entire team. Rather, the goal is to find overlapping consensus wherever you can and to be clear about what you need to de-prioritize. You want to then repeatedly refine your message so you can convince the vast majority of your team to get behind your transformation goals.

How do you know when you’ve arrived at an effective vision? John Kotter, chairman at Kotter, Inc, gives a useful rule of thumb, saying, “if you can’t communicate the vision to someone in five minutes or less and get a reaction that signifies both understanding and interest, you are not yet done with this phase of the transformation process.” Ask yourself how you fair on this front. Can you communicate your vision for data transformation in five minutes or less and get an enthusiastic, informed response? If not, you know you need to keep refining.

To get this phase right, you must be absolutely clear about the use cases that address the real pain that your customers are experiencing right now — or will experience in the future. If your vision doesn’t point to specific use cases, it will feel too abstract to be inspiring, and your vision will never be translated into reality.

To pinpoint these use cases, you might review our banking diagnostic survey data above and see which points match with your experience. Do your customers request financial guidance? Do they want to see all their finances in one place? Is your data accessible across departments? Perhaps most importantly, do your main competitors do these things?

If you’re unsure about how to answer these questions, start with surveys. Survey your user base and survey your employees. Then move onto competitive research, gathering intelligence about the features that each of your competitors offer. With this information at hand, you’ll have a set of use cases you can leverage to back up any points of possible contention — anything a detractor might throw your way. Note that you don’t necessarily have to include any of these use cases in your official presentation about your vision, but you should have them handy to show people who remain unconvinced that you have anticipated their potential concerns.

Once you have your vision nailed down, don’t overlook the critical step of communicating your vision. Too often leaders believe that once they have sent out a single memo communicating their vision, the job is done. Now the company knows. But nothing could be further from the truth. In reality, your communication — even if it’s flagged as important — will almost certainly be buried in the dozens of emails and instant messages your team members receive daily. To make a dent, you have to communicate beyond the point it feels like you’ve overdone it.

As John Kotter explains, you have to tie your daily communication back to your vision bit by bit indefinitely: “Executives who communicate well incorporate messages into their hour-by-hour activities. In a routine discussion about a business problem, they talk about how proposed solutions fit (or don’t fit) into the bigger picture. In a regular performance appraisal, they talk about how the employee’s behavior helps or undermines the vision. In a review of a division’s quarterly performance, they talk not only about the numbers but also about how the division’s executives are contributing to the transformation. In a routine Q&A with employees at a company facility, they tie their answers back to renewal goals.” So do everything in your power to promote your vision, mission, and values. Hang them on the wall in your offices. Weave them into your emails and instant messages. Mention them in company meetings. Whatever it takes.

Realize that you’ll also need to consistently update the team on the progress of the mission and the impact on both the organization and the impact on customers (including retention, satisfaction, and financial wellness, etc.).

Once you’ve built urgency and communicated your vision, you’re ready to start exploring possible solutions.

What to Offer to Build a Data Strategy

Propose Possible Solutions

Aggregation enables users to see all their accounts and transactions in one place. For example, if ACME Financial offers account aggregation, users can log in and view data from potentially anywhere they have a financial account — all through ACME Financial banking portal. In short, aggregation turns ACME Financial into a one-stop financial hub.

The process generally requires either “scraping” a financial institution’s website with algorithms that mimic human behavior or connecting directly through a data exchange. Of the two, connecting via a data exchange is a vastly better experience since it’s the fastest and most secure way to aggregate financial accounts; however, since connecting via a data exchange requires permission from each party involved, and since those parties are sometimes resistant to sharing that data, most aggregation today still occurs via data scraping.

Regardless of how it happens, data aggregation empowers both the end user and the financial institution. The end user sees all their finances in one place, and the financial institution gathers all the data it needs to best help their end users.

Data Enhancement

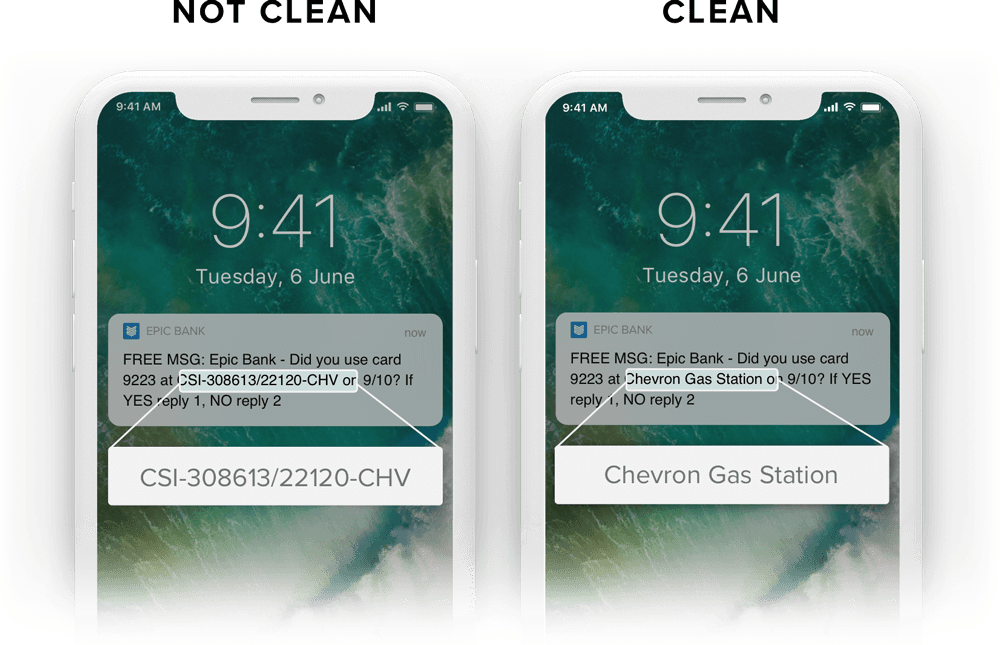

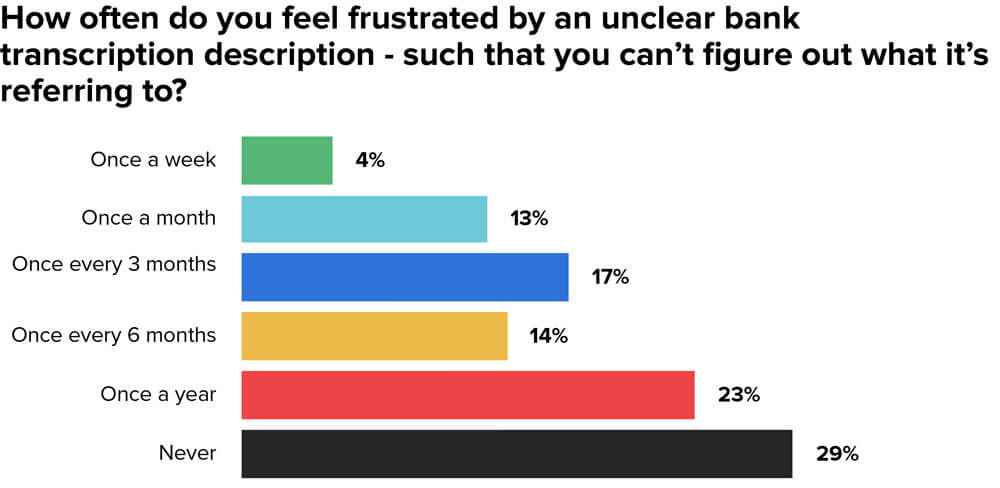

Of course, it’s not enough to just aggregate data — largely because raw transaction data is often totally incomprehensible. Who knows what a transaction description like CSI-308613/22120-CHV refers to?

MX Research, Survey of 1,000+ Employees in Financial Services

This frustration results in complaints to your call center and a negative perception of your brand. Fixing this problem can result in major cost savings. In fact, when BECU introduced data enhancement into their mobile app, the credit union’s contact center experienced a steep reduction in telephone volume — from 8.8% total call volume growth in year one to 1.5% in year three as more and more people used the enhanced mobile app.

In addition, it does little to help you understand your account holders. How can you make use of the data to empower people to be financially strong if the data isn’t clean? If you’re going to fix this problem, you’ll want transaction data that has been cleansed, categorized, and classified.

Cleanse. When your users can’t understand a transaction description, they don’t get upset with the vendor or the card provider. They get upset with you. They dial in to your call center and drain your employee’s time. You can prevent this problem by cleaning all descriptions.

Categorize. Your users are looking for help with their finances, and they don’t want to spend all their time tracking their spending habits. By adding automatic categorization to your transaction feeds, you help these account holders better manage their money while improving user loyalty, driving revenue growth, and paving the way for future technology.

Augment. When you properly classify transactions, you can see which of your users’ transactions are marked as bill pay, direct deposit, fees, and more — giving you the ability to more precisely target end users. For instance, you might target account holders who use bill pay with your competitors to use bill pay with you instead (amping up your bottom line and building value for your customers).

Enhancing transactions this way — through cleansing, categorizing, and classifying — sets the right foundation for not only a better mobile experience but also for whatever the future may bring. For instance, if you want to offer voice-assistance or AI-enabled features, you need clean data. (These features are useless without it.) As Ron Shevlin, Managing Director of Fintech Research at Cornerstone Advisors, asks, “If you don't have good data and analytics capabilities, what good will an AI-first strategy do?” You have to lay the right foundation with data before you start dreaming of an advanced user experience.

Data Analytics

Do you know how many of your account holders use your digital products at least weekly? Do you know how many have aggregated an external account? Or what percentage have a loan with you?

If you have this information, is it easily accessible — or is it buried in a database that’s difficult to view?

To transform into the digital era, you’ll want all essential data to be instantly available via a realtime dashboard. This might include tracking total users over time, external accounts per user, mobile session over time, total users with mortgages, credit card rates by institution, and much more.

Again, the point isn’t just to have this data in a database somewhere in the organization. The point is to have it on hand and ready to make use of.

Data Discovery

Once you have a 360-degree view of each user’s data, have cleansed, categorized, and classified it, and have it all available via a dynamic dashboard, you’re set to make discoveries about your client base and think about how best to position your products, services, and potential partnerships to enhance your relationship with your customers — something that many banks attempt to do but fail at in execution because their thinking is short term and focused on value extraction rather than value creation.

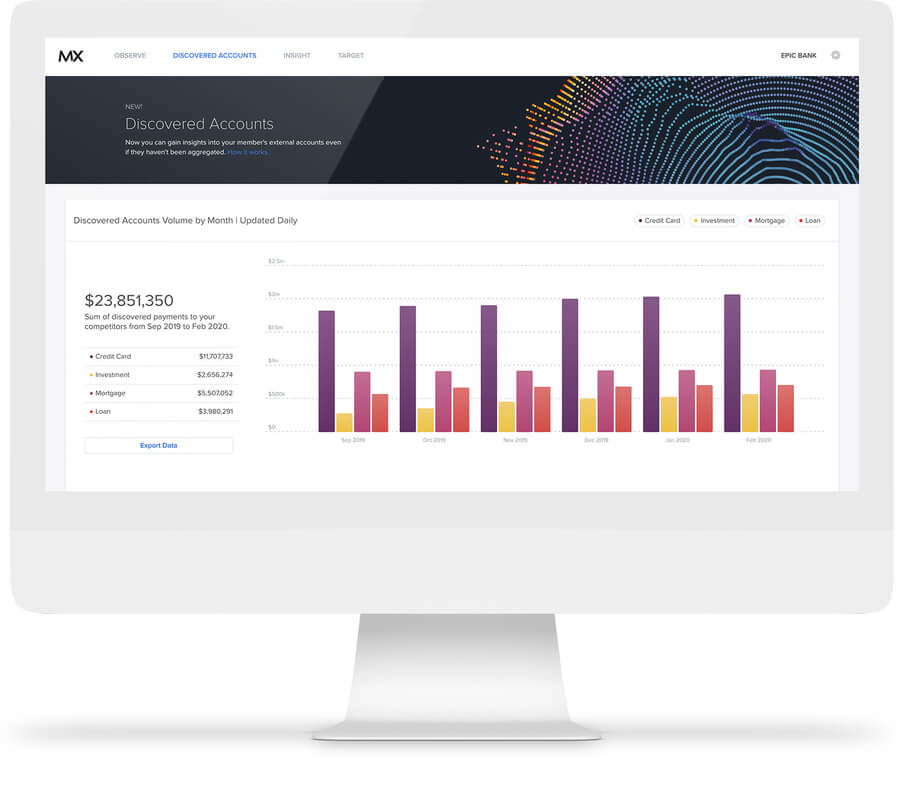

Among many things, you can learn how and when money leaves your institution to a competitor’s institution via a myriad of transaction types (including credit card and loan payments). This process, known as Discovered Accounts, sets your financial institution up to target these customers with a personalized offer that directly improves your offering compared to your competitor, encouraging customers to switch their full loyalty to your bank or credit union.

For instance, one major US bank ran a deep analysis on their users’ total card payments and found that $1.6 billion of their users’ money was going toward cards at other competing companies. This discovery enabled the bank to be more methodical about deepening their relationships with their clients. It also shows the merits behind offering consolidation loans for customers — reducing the interest rate customers are paying while increasing their own profitability.

Conclusion: Get Ready for a Data Transformation

With a sense of urgency, a vision for the future, and a solid overview of possible solutions, you’re ready to start researching specific methods (in-house or partnerships) that can give you the edge in data transformation. With the right data on hand, you can offer your customers a range of useful solutions including automated financial guidance, a personalized financial news feed, personalized offers, and much more.

The Ultimate Banker's Guide to Data Transformation

The Ultimate Banker's Guide to Data Transformation